Partnership

Sole proprietorship, limited partnership, compare businesses, employee rights, osha regulations, labor hours, personal & family, child custody & support, guardianship, incarceration, civil and misdemeanors, legal separation, real estate law, tax, licenses & permits, business licenses, wills & trusts, power of attorney, last will & testament, living trust, living will.

- Share Tweet Email Print

REAL ESTATE LAW

What is a deed of trust with assignment of rents.

By Rebecca K. McDowell, J.D.

February 24, 2020

Reviewed by Michelle Seidel, B.Sc., LL.B., MBA

Learn About Our Review Process

Our Review Process

We write helpful content to answer your questions from our expert network. We perform original research, solicit expert feedback, and review new content to ensure it meets our quality pledge: helpful content – Trusted, Vetted, Expert-Reviewed and Edited. Our content experts ensure our topics are complete and clearly demonstrate a depth of knowledge beyond the rote. We are incredibly worried about the state of general information available on the internet and strongly believe our mission is to give voice to unsung experts leading their respective fields. Our commitment is to provide clear, original, and accurate information in accessible formats. We have reviewed our content for bias and company-wide, we routinely meet with national experts to educate ourselves on better ways to deliver accessible content. For 15 years our company has published content with clear steps to accomplish the how, with high quality sourcing to answer the why, and with original formats to make the internet a helpful place. Read more about our editorial standards .

- What Is a Corporate Assignment of Deed of Trust?

A deed of trust is a written instrument granting a lien on real property. While slightly different from a mortgage, they are functionally nearly the same. Some states use deeds of trust instead of mortgages while others allow both. Either way, a deed of trust used to secure a commercial loan may also include an assignment of rents , which gives the lender the right to collect rental income from the property in the event of default.

What Is a Deed of Trust?

A deed of trust is a document that a borrower may execute in favor of a lender to give the lender a lien on a parcel of real estate. Like a mortgage, a deed of trust secures the loan by allowing the lender to foreclose on the real estate if the loan isn't paid (although in some states that use deeds of trust, a foreclosure isn't necessary).

Read More: How to Research a Deed of Trust

Deed of Trust vs. Mortgage

A deed of trust is very similar to a mortgage in that it pledges property to secure a loan. A mortgage, however, is simpler; the property owner executes a mortgage document in favor of the lender, and the lender records the mortgage and has a lien , but the property owner still holds title to the property.

A deed of trust, on the other hand, grants an actual ownership interest in the property to a trustee, who holds the property in trust for the lender until the obligation is paid.

What Is an Assignment of Rents?

An assignment of rents is extra security granted to a lender that provides a commercial loan. Commercial loans are loans that are not made for family or household use but for business purposes.

When a borrower grants a mortgage or deed of trust on real estate and the real estate has tenants who pay rent, the lender can demand an assignment of rents in addition to the mortgage or deed of trust.

The assignment of rents means that if the borrower defaults on the loan, the lender can step in and collect the rents directly from the tenants.

Deed of Trust With Assignment of Rents

A deed of trust may contain an assignment of rents clause for that same property. In addition to a clause in the deed of trust, the lender may also require the borrower to execute a separate document called an "Assignment of Rents" that is recorded with the register of deeds.

Whether the assignment is written in the deed of trust only or is also contained in a separate document, it is binding on the borrower as long as its language is clear and sufficient to create an assignment under state law.

Exercising an Assignment of Rents

When a lender decides to collect the rents on the borrower's property, the lender is said to be exercising the assignment of rents. The lender cannot exercise the assignment unless the borrower has defaulted on the loan. Once that happens, the lender can send a written demand to the tenant or tenants, requiring that the rents be paid directly to the lender.

Absolute Assignments of Rents

An assignment of rents most likely will contain language that the assignment is an absolute assignment . In most states, an absolute assignment gives the lender an immediate interest in the rents. This means that the lender actually owns the rents and is simply allowing the borrower to collect them on license until an event of default. Once a default occurs, the lender can intercept the rents without taking any court action; a letter to the tenants is all that's needed.

Every state's laws are different; the law of the state where the property is located will dictate how a lender can exercise an assignment of rents.

Read More: What Is the Difference Between a Deed and a Deed of Trust?

- Companies Incorporated: Mortgage States and Deed of Trust States

- American Bar Association: Commercial Real Estate FAQs

- Schulte Roth & Zabel: Sixth Circuit Upholds Assignment of Rents to Secured Lender

- Findlaw: California Civil Code - CIV § 2938

- Legal Beagle: What Is the Difference Between a Deed and a Deed of Trust?

- Legal Beagle: How to Research a Deed of Trust

- Legal Beagle: Documents Needed to Refinance a Mortgage

- Legal Beagle: How to File a Property Lien

Rebecca K. McDowell is a creditors' rights attorney with a special focus on bankruptcy and insolvency. She has a B.A. in English from Albion College and a J.D. from Wayne State University Law School. She has written legal articles for Nolo and the Bankruptcy Site.

Related Articles

- Who Can Act As Trustee in a Texas Deed of Trust?

- The Definition of a Leasehold Deed of Trust

- How to Waive Right of Redemption After Foreclosure

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

NerdWallet, Inc. is an independent publisher and comparison service, not an investment advisor. Its articles, interactive tools and other content are provided to you for free, as self-help tools and for informational purposes only. They are not intended to provide investment advice. NerdWallet does not and cannot guarantee the accuracy or applicability of any information in regard to your individual circumstances. Examples are hypothetical, and we encourage you to seek personalized advice from qualified professionals regarding specific investment issues. Our estimates are based on past market performance, and past performance is not a guarantee of future performance.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

Deed of Trust: Definition, Uses

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

The investing information provided on this page is for educational purposes only. NerdWallet, Inc. does not offer advisory or brokerage services, nor does it recommend or advise investors to buy or sell particular stocks, securities or other investments.

Table of Contents

Deeds of trust vs. mortgages

How does a deed of trust work, deed of trust by state, deeds of trust vs. warranty deeds.

A deed of trust is a real estate transaction agreement that allows a third-party trustee to hold the property title until the borrower repays the lender in full. The third party in a deed of trust is typically a title company or real estate broker [0] Cornell Law School Legal Information Institute . Deed of Trust . Accessed Jun 1, 2023. View all sources .

Over half of states use deeds of trust instead of mortgages , which involve only two parties. However, in many states, home loans are colloquially referred to as “mortgages,” although they may legally be deeds of trust.

The main difference between a mortgage and a deed of trust is that if you fall behind on loan payments, the property can be foreclosed on more quickly with a deed of trust than with a mortgage.

A deed of trust is not to be confused with a living trust , which is an estate planning tool that helps avoid probate. It also doesn’t transfer ownership of the real property as a property deed does.

Deeds of trust and mortgages are lending agreements that place a lien, or legal claim until debt repayment, on real property. Here’s how they’re similar:

They’re subject to state laws.

Both are public record.

Both allow for foreclosure.

Both are considered contracts as opposed to loans.

However, there are two key differences:

Number of parties involved. A mortgage involves two parties: the lender and the borrower, while a deed of trust involves three parties: the lender, the borrower and the trustee.

Foreclosure type and time. Mortgages typically have to go through a judicial foreclosure, while deeds of trust generally can use a nonjudicial foreclosure process without involving the courts. Because a nonjudicial foreclosure process tends to be faster and less expensive than a judicial one, it usually takes less time and effort to foreclose with a deed of trust than with a mortgage.

As a home buyer, you don’t have the option to choose between a mortgage or a deed of trust, even if you live in one of the nine states that allow both. In those states, the lender chooses which document to use.

A deed of trust works similarly to a mortgage by making a piece of real property the collateral for a loan. This means that if you don’t make your loan payments on time, your lender can foreclose on the property. Unlike a mortgage, though, a deed of trust typically allows for foreclosure without the need to first obtain a court order.

Here’s how the process works:

The trust deed includes a promissory note that spells out the exact terms of the loan including the principal, interest, occupancy, insurance and maintenance requirements. The borrower signs this note, agreeing to repay the borrowed money.

The trustee holds legal ownership of the property or in some states just holds the lien, which is a legal claim to the asset, but has no control over that property unless the borrower doesn’t make their scheduled payments per the terms of the agreement.

While the buyer is making payments, the lender keeps the promissory note. Once the loan is paid off, however, the promissory note is marked “paid in full” and the deed is returned to the buyer. At this point, the buyer will own the property outright.

Requirements to create a deed of trust

A valid deed of trust must always involve three parties:

The borrower, also known as the trustor.

The lender, also known as the beneficiary .

The trustee, which is typically a title company that holds legal title to the real property or, in some states, just holds the lien.

The deed of trust document should contain the following information:

The names of all the involved parties (borrower, lender and trustee).

A description of the property involved.

The original amount of the loan.

Loan inception and maturity dates.

Any fees or riders involved.

What will happen in the event of loan default.

Depending on the nature of the sale, any other relevant details.

The following states (and Washington, D.C.) use deeds of trust instead of mortgages:

California.

Massachusetts.

Mississippi.

New Hampshire.

New Mexico.

North Carolina.

Rhode Island.

Washington.

West Virginia.

Deeds of trust and mortgages are allowed in these states:

South Dakota.

All remaining states use only mortgages:

Connecticut.

New Jersey.

North Dakota.

Pennsylvania.

South Carolina.

A warranty deed is a document required by some lenders before they approve financing. It certifies that the seller is the true owner of the property and has the right to sell it and that there are no outstanding debts, liens, judgments or encumbrances on the property.

A deed of trust is a lending contract, while a warranty deed is offered by a seller to a buyer for the buyer’s protection.

You can deduct your loan interest payments on your income tax return for home mortgages and deeds of trust. To do so, just be sure the property has been recorded as your principal residence in your county records [0] IRS.gov . Publication 936 (2022), Home Mortgage Interest Deduction . Accessed Jun 1, 2023. View all sources .

If you have a loan secured by a deed of trust and your lender sells that trust deed, an assignment of trust deed assigns that deed of trust to the new buyer of your loan (typically another lender). The assignment of deed of trust grants the new loan purchaser all rights to the property and is recorded as public record along with the original deed of trust.

A reconveyance in a deed of trust is a transfer of property (minus the lien) to the borrower from the trustee or the lender. This happens when the borrower has paid off the loan and satisfied the terms of the debt, and it means the lender no longer has an interest in the property.

You can deduct your loan interest payments on your income tax return for home mortgages and deeds of trust. To do so, just be sure the property has been recorded as your principal residence in your county records

On a similar note...

Compare online will makers

Assignment of Deed of Trust Vs. Deed or Grant Deed

A grant deed is used to transfer ownership rights in real estate.

Jupiterimages/liquidlibrary/Getty Images

More Articles

- 1. What Is the Difference Between the Deed of Absolute Sale and the Deed of Assignment?

- 2. What is an Assignment of Trust Deed?

- 3. Warranty Deed Vs. Deed of Trust

Property rights in real estate are valuable and invariably the subject of a legal document called a deed. To transfer ownership rights in real estate, a grant deed is commonly used. When a loan is obtained to purchase real estate, a deed of trust is often used to give the lender rights in the real estate to secure repayment of the loan. An assignment of deed of trust is used by a lender when it sells its loan secured by a deed of trust.

Property Deeds

Real estate transactions that involve the transfer of property rights require a deed to ensure the transfer of rights is effective. All deeds are written documents that include a description of the affected real estate and the names of the persons whose property rights are being transferred. Although not legally require to make the transfer effective, deeds are routinely recorded with the local government office responsible for recording real estate transactions. A recorded deed gives the public notice regarding property rights in a particular parcel of real estate, such as ownership, easements and liens. Recording a deed can also protect a property owner against future claims that his property rights are invalid.

A grant deed is used to transfer real estate ownership from one person to another. The transfer of ownership can be for a full parcel of real estate or just a portion of the real estate. Grant deeds are most often used in real estate sales between an unrelated buyer and seller. However, a grant deed may also be used to transfer ownership as a gift. When a grant deed is used, the person transferring ownership rights is promising to the person receiving ownership rights that these rights have not been previously transferred to anyone else.

Deed of Trust

A deed of trust is used in a three-party transaction involving the repayment of a debt. The first party is a real estate owner or buyer who is borrowing money that can be used for any purpose, but is typically used to fund the purchase of the real estate. The second party is the lender, such as a bank or other financial institution, providing the funds to the borrower. To secure repayment of the loan, the borrower signs a deed of trust which transfers legal title to his real estate to a third party, called the trustee, who can be any individual or company that does not have any interest in the loan or real estate. The borrower continues to have the beneficial use of the property with the trustee only taking action if the borrower defaults on his loan. If the lender and borrow cannot work out a resolution of the default, the lender can instruct the trustee to conduct a foreclosure sale of the real estate and deliver the sale proceeds to the lender to repay the loan.

Assignment of Deed of Trust

Loans that are secured by a deed of trust often include repayment terms that extend for several years or more. From a lender’s perspective, a loan secured by a deed of trust is a fairly safe investment when the value of the real estate is sufficient to repay the loan in the event of a borrower's default. This aspect makes existing loans secured by a deed of trust suitable for sale from the original lender to another lender during the life of the loan. To complete the sale of a loan secured by a deed of trust, the original lender uses a document called an assignment of deed of trust to transfer its rights in the deed of trust to a new lender.

- FindLaw: What Are Property Deeds?

- Cornell University Law School Legal Information Institute: Deed of Trust

- California Department of Real Estate: Trust Deed Investments -- What You Should Know?

Joe Stone is a freelance writer in California who has been writing professionally since 2005. His articles have been published on LIVESTRONG.COM, SFgate.com and Chron.com. He also has experience in background investigations and spent almost two decades in legal practice. Stone received his law degree from Southwestern University School of Law and a Bachelor of Arts in philosophy from California State University, Los Angeles.

Related Articles

What is the difference between the deed of absolute sale and the deed of assignment, what is an assignment of trust deed, warranty deed vs. deed of trust, land sale contract vs. trust deed, what is the redemption period in tennessee, what is the collateral assignment of a life insurance policy, how to assume a promissory note, transferring a deed of trust to a granddaughter, owner finance laws, definition of 'trustee' in real estate, certificate of title vs. deed, foreclosure right of redemption & tenant's rights in maryland.

Zacks Research is Reported On:

Zacks Investment Research

is an A+ Rated BBB

Accredited Business.

Copyright © 2024 Zacks Investment Research

At the center of everything we do is a strong commitment to independent research and sharing its profitable discoveries with investors. This dedication to giving investors a trading advantage led to the creation of our proven Zacks Rank stock-rating system. Since 1986 it has nearly tripled the S&P 500 with an average gain of +26% per year. These returns cover a period from 1986-2011 and were examined and attested by Baker Tilly, an independent accounting firm.

Visit performance for information about the performance numbers displayed above.

NYSE and AMEX data is at least 20 minutes delayed. NASDAQ data is at least 15 minutes delayed.

Legal Dictionary

The Law Dictionary for Everyone

Deed of Trust

A deed of trust is an agreement that is made between a lender and a borrower, to allow a neutral third party to act as a trustee over a piece of property. The trustee holds legal title to the property until the borrower can pay off his debt. As he repays the debt, the borrower keeps the actual title to (and possession of) the property, and maintains full responsibility over the premises, unless the deed of trust says otherwise. The legal title to the property, however, is held by the trustee. To explore this concept, consider the following deed of trust definition.

Definition of Deed of Trust

- A document that secures a debt, in which a debtor places legal ownership of real property with a trustee, to be held in trust until the debt is repaid.

What is a Dead of Trust

A deed of trust is a legal document that a borrower and a lender agree to make, which permits a neutral third party to enter the fold as a trustee over a piece of real property. For example, the deed of trust permits the trustee to hold onto the property while the borrower repays his debt. During this time, the borrower keeps the actual title to the property, and remains fully responsible for the property. The trustee, on the other hand, holds on to the legal title.

Deeds of trust have become less popular as more people have opted for mortgages. One of the main differences between a deed of trust and a mortgage is that, with a mortgage, everyone involved in the transaction has a vested interest in the outcome of the arrangement. With a deed of trust, an impartial third party serves as trustee. For example, a deed of trust can only be sold by the trustee, who is not permitted to change the selling price to benefit either the borrower or lender.

Once the sale of a property under a deed of trust is finalized, the trustee distributes the proceeds to the lender, with the remainder to the borrower. The lender receives the amount necessary to fully satisfy the debt, and the borrower receives whatever is left over.

The term “trustee” refers to any person who is in a position of trust, responsibility, or authority for the benefit of another person. A trustee is “trusted” with another person’s property. Trustees may be responsible for carrying out certain tasks, but without the benefit of earning an income for their efforts. When it comes to real property, a trustee is a holder of the property, typically on behalf of a beneficiary . This means that the trustee holds the property for the beneficiary until the beneficiary is ready to take the property over.

Difference Between Deed of Trust and Mortgage

In order to better understand the difference between a deed of trust and a mortgage, it is important to first define promissory notes. A promissory note does as its name suggests: it contains a “promise” on the part of the borrower to repay the amount he is borrowing. A promissory note is essentially an IOU. Both mortgages and deeds of trust are considered promissory notes, and both use real property to secure the loan. This means that, if the borrower fails to make his monthly payments, the lender is permitted to foreclose on the property, based on the promise in the mortgage or deed of trust having been broken.

Many people believe that a mortgage is the loan that they take out on their property, but this is not actually true. The mortgage is the document that the borrower gives to the lender to allow the lender to place a lien on his property. If a property owner is unsure as to whether he has a mortgage or a deed of trust, the borrower can review the documents he received when the property was initially sold to him. The only time the difference between a deed of trust and a mortgage becomes an issue is if the property goes into foreclosure . This is because the foreclosure process is different for a property under deed of trust.

Foreclosure

Another difference between a deed of trust and a mortgage is the foreclosure process. A foreclosure is the sale of a piece of property by a lender when a borrower has failed to make his loan payments as agreed. The lender then sells the property to recoup what is owed so that the loan can be fully satisfied.

When a piece of property under a deed of trust goes into foreclosure, the foreclosure sale does not have to adhere to the same procedures that a foreclosure on a mortgaged property must heed. With a foreclosure on a mortgaged property, the rules are stricter, and the parties involved are held to a higher level of accountability. A foreclosure sale under a deed of trust, however, does not require court intervention in most states.

Power of Sale

A power of sale is a clause found in most deeds of trust that allow a trustee to sell the property if the borrower defaults on his loan, and the property goes into foreclosure. The courts have consistently held that a deed of trust with a power of sale clause effectively serves as the property owner’s permission for a trustee to conduct a nonjudicial foreclosure in the event that the borrower defaults on his payments. What this means is that the lender does not need to sue the borrower in state court. Instead, the lender instructs the trustee to mail or serve the required notices that the property will be auctioned off at a “trustee’s sale.”

Once the property is sold at the trustee’s sale, the borrower’s title is automatically terminated. The trustee then issues a deed transferring the legal title to the property to the highest bidder. The bidder then records that deed and becomes the new owner of record. This is why lenders prefer deeds of trust over mortgages. They can sell the property much more quickly, recovering the collateral of the loan without needing to incur the expenses that would be involved with suing the borrower.

The length of time that it takes to complete a trustee’s sale – or power of sale foreclosure – varies wildly, depending on the jurisdiction . Some states, like Virginia, have incredibly short time lines, Virginia’s being only two weeks. The process begins only when the lender or trustee records a notice of default, no matter how long the borrower has been in default on his payments. Poor economic conditions have also influenced states to extend the time in which to sell the property, understanding that it may take longer than usual to do so in a struggling economy.

Deed of Trust Form

For borrowers who wish to conduct their own real estate transactions, they can use a free deed of trust form, which can be found on the internet. They must file the completed and signed deed of trust form with the county clerk within the jurisdiction of their property. Filing the deed of trust form with the county clerk is crucial because the filing itself acts as a sort of notice to any interested parties that the property is being purchased under a deed of trust.

Assignment of Deed of Trust

An assignment of deed of trust transfers the interest that the original borrower had under the deed of trust to a new bank. Typically, the deed of trust is recorded shortly after the lender signs it. If further assignments of deed of trust are to follow, each must be recorded with the county clerk.

Lenders buy and sell loans all the time, with usually little to no effect on the borrower. The assignment of deed of trust simply serves as permission for one lender to sell the loan to another lender. Once the loan is re-assigned, the new lender takes over the same lien on the same piece of property, essentially stepping into the shoes of the prior lender. The borrower can be provided with a copy of the assignment of deed of trust upon repaying his debt in full.

Deed of Trust Example Concerning an Assignment of Deed of Trust

An example of a deed of trust action can be found in the case of Maria Mendoza v JPMorgan Chase Bank. In November of 2007, Maria and Juan Mendoza took out a loan in the amount of $540,600 from JPMorgan Chase Bank. The loan was secured by a deed of trust. In the loan, the Mendozas were listed as the borrowers, Chase as the lender and beneficiary, and North American Title Company as the trustee. Unfortunately, by March of 2011, the Mendozas had fallen behind on their payments – to the tune of nearly $55,000.

On March 4, 2011, Chase reassigned the deed of trust to Chase Home Finance, LLC. California Reconveyance Company then replaced North American Title Company as the trustee on the loan. California Reconveyance Company issued a notice to the Mendozas indicating their default on the loan and the trustee’s intention to sell the property. Maria Mendoza filed a lawsuit challenging the assignment of the deed of trust, as well as the substitution of California Reconveyance Company as trustee.

Mendoza’s argument was that Colleen Irby, who had signed the assignment as an officer of Chase, was actually an employee of California Reconveyance Company. Mendoza had gleaned this information from Irby’s LinkedIn.com page, where she identified herself as an employee of the latter. Mendoza therefore alleged that Irby acted fraudulently in performing the assignment. Mendoza accused Irby of being a “robo-signer,” which is someone who simply signs documents, with no legal authority whatsoever. Mendoza argued that the substitution of the trustee was equally fraudulent.

The defendants filed a motion to dismiss , which was ultimately granted by the trial court. Mendoza then appealed to California’s Court of Appeals for the Third District. The Court of Appeals ultimately affirmed the dismissal primarily because Mendoza failed to provide enough factual evidence in her complaint , and in her appeal . The court explained its decision, stating:

“We uphold the trial court’s ruling because plaintiff lacks standing to challenge the assignment of her loan and deed of trust. Plaintiff makes the rote assertion that if afforded the opportunity, she would provide more facts to coincide with the emerging jurisprudence . That promise does not meet her burden of disclosing in her briefing what new facts she can now state to revive her wrongful foreclosure claim. As a result, the trial court did not abuse its discretion by foreclosing additional amendments.”

The Court concluded by saying that:

“[Mendoza] offers no new factual allegations to merit an opportunity to further amend her complaint or to demonstrate that the trial court abused its discretion. She has had three opportunities to state a viable claim against these defendants and has fallen far short of the mark.”

Related Legal Terms and Issues

- Collateral – Something of value pledged as security for repayment of a loan.

- Defendant – A party against whom a lawsuit has been filed in civil court, or who has been accused of, or charged with, a crime or offense.

- Lien – An encumbrance placed on a person’s property to secure a debt the property owner owes to another person or entity.

- Promissory – Containing, implying, or having the nature of a promise.

- Search Search Please fill out this field.

What Is a Trust Deed?

Understanding trust deeds, trust deed vs. mortgage, what is included in a trust deed, foreclosures and trust deeds.

- Investing in Trust Deeds

- Real-World Example

The Bottom Line

- Personal Finance

Trust Deed: What It Is, How It Works, Example Form

:max_bytes(150000):strip_icc():format(webp)/troypic__troy_segal-5bfc2629c9e77c005142f6d9.jpg "deed of trust and assignment")

A trust deed —also known as a deed of trust —is a document sometimes used in real estate transactions in the U.S. It is a document that comes into play when one party has taken out a loan from another party to purchase a property. The trust deed represents an agreement between the borrower and a lender to have the property held in trust by a neutral and independent third party until the loan is paid off.

Although trust deeds are less common than they once were, some 20 states still mandate the use of one, rather than a mortgage , when financing is involved in the purchase of real estate. Trust deeds are common in Alaska, Arizona, California, Colorado, Idaho, Illinois, Mississippi, Missouri, Montana, North Carolina, Tennessee, Texas, Virginia, and West Virginia.

A few states—such as Kentucky, Maryland, and South Dakota—allow the use of both trust deeds and mortgages.

Key Takeaways

- In financed real estate transactions, trust deeds transfer the legal title of a property to a third party—such as a bank, escrow company, or title company—to hold until the borrower repays their debt to the lender.

- Trust deeds are used in place of mortgages in several states.

- Investing in trust deeds can provide a high-yielding income stream.

Investopedia / Danie Drankwalter

A trust deed is a transaction between three parties:

- Lenders , officially known as beneficiaries . These are the interests a trust is supposed to protect.

- A borrower , otherwise known as a trustor . This is the person who establishes a trust.

- A trustee , a third party charged with holding the entrusted property until a loan or debt is paid for in full.

In a real estate transaction—the purchase of a home, say—a lender gives the borrower money in exchange for one or more promissory notes linked to a trust deed. This deed transfers legal title to the real property to an impartial trustee , typically a title company, escrow company, or bank, which holds it as collateral for the promissory notes . The equitable title — the right to obtain full ownership — remains with the borrower, as does full use of and responsibility for the property.

This state of affairs continues throughout the repayment period of the loan. The trustee holds the legal title until the borrower pays the debt in full, at which point the title to the property transfers to the borrower. If the borrower defaults on the loan, the trustee takes full control of the property.

Trust deeds and mortgages are both used in bank and private loans for creating liens on real estate, and both are typically recorded as debt in the county where the property is located. However, there are some differences.

Number of Parties

A mortgage involves two parties: a borrower (or mortgagor) and a lender (or mortgagee). When a borrower signs a mortgage, they pledge the property as security to the lender to ensure repayment.

In contrast, a trust deed involves three parties: a borrower (or trustor), a lender (or beneficiary), and the trustee. The trustee holds title to the lien for the lender's benefit; if the borrower defaults, the trustee will initiate and complete the foreclosure process at the lender's request.

Type of Foreclosure

In the event of default, a deed of trust will result in different foreclosure procedures than a mortgage. A defaulted mortgage will result in a judicial foreclosure, meaning that the lender will have to secure a court order. Trust deeds go through a non-judicial foreclosure, provided that they include a power-of-sale clause.

Judicial foreclosures are more expensive and time-consuming than non-judicial foreclosures. This means that in states that allow them, a deed of trust is preferable to a mortgage from the lender's point of view.

Contrary to popular usage, a mortgage is not technically a loan to buy a property; it's an agreement that pledges the property as collateral for the loan.

A deed of trust will include the same type of information stated in a mortgage document, such as:

- The identities of the borrower, lender, and trustee

- A full description of the property to be placed in trust

- Any restrictions or requirements on the use of the property while it is in trust

- The terms of the loan, including principal, monthly payments, and interest rate

- The terms of any late fees and penalties in the event of repayment

In addition, a trust deed will also include a power of sale clause that gives the trustee the right to sell the property if the borrower defaults.

Mortgages and trust deeds have different foreclosure processes. A judicial foreclosure is a court-supervised process enforced when the lender files a lawsuit against the borrower for defaulting on a mortgage. The process is time-consuming and expensive.

Also, if the foreclosed-property auction doesn't bring in enough money to pay off the promissory note, the lender may file a deficiency judgment against the borrower, suing for the balance. However, even after the property is sold, the borrower has the right of redemption : they may repay the lender within a set amount of time and acquire the property title.

In contrast, a trust deed lets the lender commence a faster and less-expensive non-judicial foreclosure, bypassing the court system and adhering to the procedures outlined in the trust deed and state law. If the borrower does not make the loan current, the property is put up for auction through a trustee's sale.

The title transfers from the trustee to the new owner through the trustee's deed after the sale. When there are no bidders at the trustee sale, the property reverts to the lender through a trustee's deed. Once the property is sold, the borrower has no right of redemption.

Furthermore, a trustee has the responsibility of paying the proceeds from the sale to the borrower and lender after the sale is finalized. The trustee will pay the lender the amount left over on the debt and pay the borrower anything that surpasses that amount, thereby allowing the lender to purchase the property.

Pros and Cons of Investing in Trust Deeds

Investors who are searching for juicy yields sometimes turn to the real estate sector—in particular, trust deeds.

In trust deed investing, the investor lends money to a developer working on a real estate project. The investor's name goes on the deed of trust as the lender. The investor collects interest on his loan; when the project is finished his principal is returned to him in full. A trust deed broker usually facilitates the deal.

High-yielding income stream

Portfolio diversification

Illiquidity

No capital appreciation

What sort of developer enters this arrangement? Banks are often reluctant to lend to certain types of developments, such as mid-size commercial projects—too small for the big lenders, too big for the small ones—or developers with poor track records or too many loans. Cautious lenders may also move too slowly for developers up against a tight deadline for commencing or completing a project.

Developers like these are often in a bit of a crunch. For these reasons, trust deed investors may often expect high-interest rates on their money. They can reap the benefits of diversifying into a different asset class, without having to be experts in real-estate construction or management. This is a form of passive investment .

Trust deed investing has certain risks and disadvantages. Unlike stocks, real estate investments are not liquid , meaning investors cannot retrieve their money on demand. Also, investors can expect only the interest the loan generates; any additional capital appreciation is unlikely.

Invested parties may exploit any legal discrepancies in the trust deed, causing costly legal entanglements that may endanger the investment. The typical investor with little experience may have difficulty, as it takes specific expertise to find credible and trustworthy developers, projects, and brokers.

Real-World Example of a Trust Deed

A short form deed of trust document used in Austin County, Texas , covers the requirements for most lenders. The form begins with a definition of terms and spaces for the borrower, lender, and trustee to fill in their names. The amount being borrowed and the address of the property are also required.

After this section, the document goes on to specify the transfer of rights in the property and uniform covenants including:

- Details about payment of principal and interest

- Escrow funds

- Property insurance and structure maintenance

- Structure occupancy—stipulating the borrower must take up residency within 60 days

The form also includes nonuniform covenants, which specify default or breach of any of the agreement terms. And it specifies that the loan the document deals with is not a home equity loan —that is, something the borrower will receive cash from—but one for purchasing the property.

The deed of trust ends with a space for the borrower's signature, which must be done in the presence of a notary and two witnesses, who also sign.

What Is Assignment in a Deed of Trust?

In real estate law, " assignment " is simply the transfer of a deed of trust from one party to another. This usually happens when the beneficiary of a trust deed sells their loan to another lender.

What Is Reconveyance in a Deed of Trust?

In real estate law, reconveyance means the transfer of a property from a lender or trustee to a borrower. This usually happens at the end of a mortgage or other loan, when the borrower has satisfied the terms of their debt.

Who Can Be a Trustee in a Deed of Trust?

Some states have laws limiting who can act as a trustee in a deed of trust. In these states, the trustee must be a bank, credit union, thrift, title insurance company, attorney, or other company specifically authorized to hold a trust. In other states, anyone can act as a trustee.

Trust deeds are an alternative to mortgages in certain states. Instead of an agreement directly between a lender and a borrower, a trust deed places the title of a property in the hands of a third party, or trustee. Only after the borrower has satisfied the terms of their debt to the lender will the property be fully transferred to the borrower.

Rocket Lawyer. " Which States Allow Deeds of Trust? "

Legal Information Institute. " Non-judicial Foreclosure ."

Legal Zoom. " Naming a Trustee in Your Deed of Trust ."

- Foreclosure: Definition, Process, Downside, and Ways To Avoid 1 of 35

- Saving Your Home From Foreclosure 2 of 35

- Workout Agreement: What it is, How it Works 3 of 35

- Mortgage Forbearance Agreement: Definition, Purpose, How It Works 4 of 35

- Short Refinance Definition 5 of 35

- Pre-foreclosure: How it Works in Real Estate, FAQs 6 of 35

- Delinquent Mortgage: What it Means, How it Works 7 of 35

- How Many Mortgage Payments Can I Miss Before Foreclosure? 8 of 35

- When to Walk Away From Your Mortgage 9 of 35

- The 6 Phases of Foreclosure 10 of 35

- Judicial Foreclosure: What it is, How it Works 11 of 35

- What Is a Sheriff's Sale? When It's Used, Process, and Proceeds 12 of 35

- What Are Your Legal Rights in a Foreclosure? 13 of 35

- How to Get a Mortgage After Bankruptcy and Foreclosure 14 of 35

- How to Buy a Foreclosed Home 15 of 35

- Successful Foreclosure Investing Strategies 16 of 35

- The Guide to Investing in REO Properties 17 of 35

- Should You Buy a House at Auction? 18 of 35

- Essential Tips for Buying a HUD Home 19 of 35

- Absolute Auction: What it is, How it Works, Example 20 of 35

- Bank-Owned Property 21 of 35

- Deed in Lieu of Foreclosure: Meaning and FAQs 22 of 35

- Basics of a Distress Sale, Why It Often Leads to Financial Loss 23 of 35

- Notice of Default: Meaning, Overview, Special Considerations 24 of 35

- Other Real Estate Owned (OREO): What it is, How it Works 25 of 35

- Power of Sale: What it is and how it Works 26 of 35

- Principal Reduction: What it is, How it Works 27 of 35

- Real Estate Owned (REO) Definition, Advantages, and Disadvantages 28 of 35

- Right of Foreclosure: Meaning, Types, FAQs 29 of 35

- Right of Redemption Definition and How to Exercise the Right 30 of 35

- Tax Lien Foreclosure: Definition, How It Works, Vs. Tax Deed Sale 31 of 35

- Trust Deed: What It Is, How It Works, Example Form 32 of 35

- Voluntary Foreclosure: Meaning, Pros and Cons, Example 33 of 35

- Writ of Seizure and Sale: What it is, How it Works 34 of 35

- Zombie Foreclosure: What It Is, How It Works 35 of 35

:max_bytes(150000):strip_icc():format(webp)/CreditKarmaHomeTheBalanceDesktop-5ce0ca77a10445b98f7bc73d4e37580b.jpg "deed of trust and assignment")

- Terms of Service

- Editorial Policy

- Privacy Policy

- Your Privacy Choices

- LEGAL GLOSSARY

More results...

- Browse By Topic – Start Here

- Self-Help Videos

- Documents & Publications

- Find A Form

- Download E-Books

- Community Organizations

- Continuing Legal Education (MCLE)

- SH@LL Self-Help

- Free Legal Consultation (Lawyers In The Library)

- Ask a Lawyer

- Onsite Research

- Interlibrary Loan

- Document Delivery

- Borrower’s Account

- Book Catalog Search

- Passport Services

- Contact & Hours

- Library News

- Our Board of Trustees

- My E-Commerce Account

SacLaw Library

Www.saclaw.org.

- Documentary Transfer Tax

- Identifying grantors and grantees

- Free Sources

- Community Resources

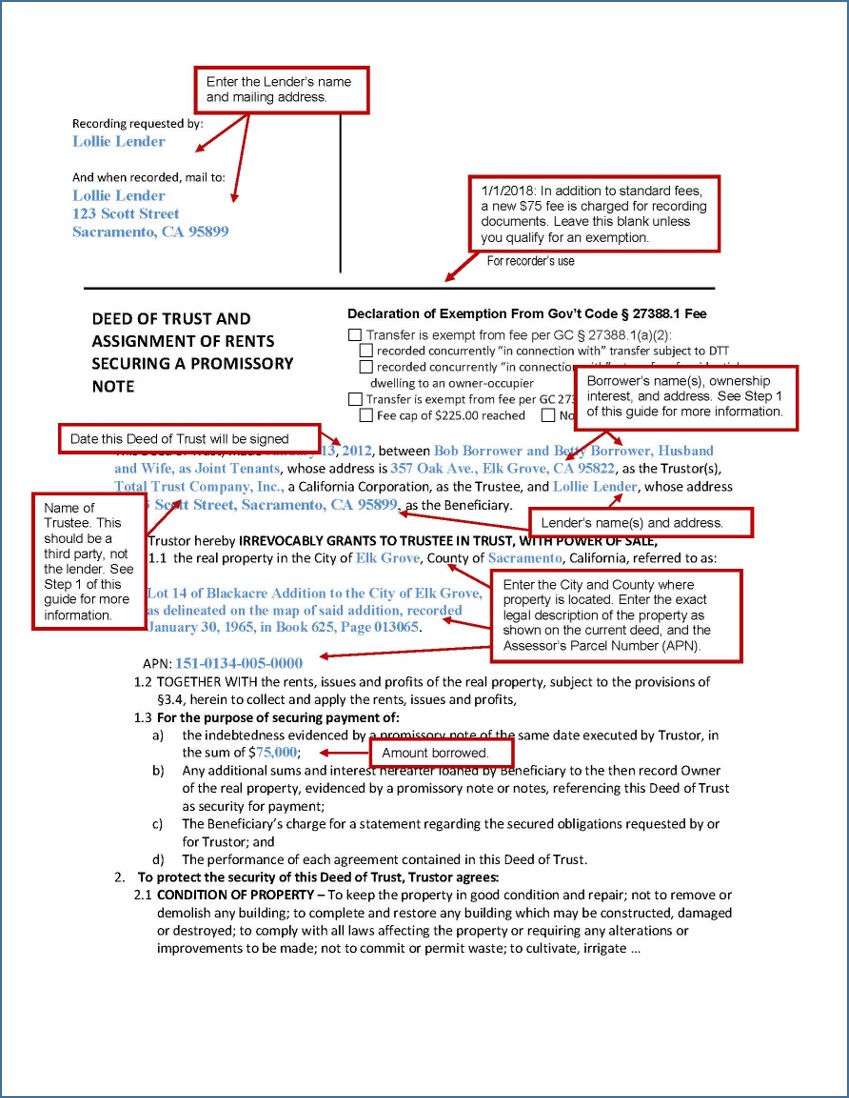

Deed of Trust and Promissory Note

Templates and forms.

A deed of trust, also called a trust deed, is the functional equivalent of a mortgage. It does not transfer the ownership of real property, as the typical deed does. Like a mortgage, a trust deed makes a piece of real property security (collateral) for a loan. If the loan is not repaid on time, the lender can foreclose on and sell the property and use the proceeds to pay off the loan.

Deed of trust is not used for transferring property to a trust A trust deed is not used to transfer property to a living trust (use a Grant Deed for that). Other than the terminology, trust deeds and living trusts have nothing in common. A living trust is used to avoid probate, not to provide security for a loan. Visit our page on Estate Planning for more information on that topic.

A trust deed is always used together with a promissory note (also called “prom note”) that sets out the amount and terms of the loan. The property owner signs the note, which is a written promise to repay the borrowed money.

A trust deed gives the third-party “trustee” (usually a title company or real estate broker) legal ownership of the property. This means that the trustee has no control over the property as long as the borrower (aka property owner or “trustor”) makes the agreed-upon loan payments and keeps the other promises in the trust deed. If the borrower defaults, however, the trustee has the power to sell the property to pay off the loan without having to file an action in court. The lender (also known as “beneficiary”) is then repaid from the proceeds.

Step-by-Step Instructions

Determine the parties to the agreement.

There will be three parties to these agreements. Identifying these parties ahead of time will make it easier to complete the forms.

Beneficiary

The beneficiary, more commonly known as the lender, is the person or company that lends the borrower money, and who will be entitled to be repaid from the proceeds of a foreclosure. If the lender is a corporation, be sure to include language such as “Lender is a corporation organized and existing under the laws of California” in your documents.

Borrower(s)

If there are two or more borrowers, they will be borrowing the money “jointly and severally.” This means each debtor is responsible (liable) for the entire amount of the debt. A creditor may collect from whichever debtor has the “deep pocket” (lots of money); the debtor who pays may demand contributions from the other debtors. Joint borrowers will want to carefully consider whether or not they wish to be jointly responsible with their co-borrower.

When the property used as security for the loan is owned by more than one person, you may want to consider who you will name as borrowers and owners of the property on the deed of trust. The names of all owners of the property, and their spouses, must be included to give the entire property (all owners’ interests in the property) as security. A co-owner can only give as security his or her interest in the property. In other words, a lender wants to be sure that all owners and their spouses sign the deed of trust as a condition of lending the money (unless the lender is willing to take as security one co-owner’s interest in property).

When a bank or savings and loan finances the purchase of real estate, the trustee is almost always a title or trust company. Sometimes real estate brokers act as trustees. Attorneys commonly write in the name of a title company as trustee on a trust deed, without consulting the title company. Title companies even give out trust deed forms with their names already printed in the “trustee” space. They don’t mind being named as trustee because a trustee has nothing to do unless the borrower defaults. If that happens, most title or escrow companies turn the deed over to a professional foreclosure firm.

Prepare the Deed of Trust and Promissory Note

The Deed of Trust and Promissory Note must be in a format that the Sacramento County Clerk/Recorder’s Office will accept. Customizable templates may be downloaded from these links:

- Promissory Note

- Deed of Trust

Sample filled-in forms with instructions are available at the end of this Guide.

Get the Signatures Notarized

Notarization is required before recording these documents with the County Recorder. The notary’s acknowledgment of the trustor’s signature is formal proof that the signature is genuine. You can find a notary at your bank, a mailing service, or in the Yellow Pages. with instructions are available at the end of this Guide.

Record the Signed Documents at the County Recorder’s Office

Take the original signed and notarized Deed of Trust and Promissory Note to the County Recorder’s Office for the county where the property is located. In Sacramento, this is at 3636 American River Drive, Ste. 110, Sacramento CA 95864. You will need to pay a fee (you can check the current recording fees in Sacramento ). The clerk in the recorder’s office will take your original documents and stamp them with the date, time, a filing number, and book and page numbers. The original documents will be mailed back to you. Note: trust deeds are exempt from the documentary transfer tax. California Revenue and Taxation Code § 11921 .

What Happens Next?

If the borrower pays off the loan without defaulting (as happens in most cases), the beneficiary (lender) will request the trustee execute and record a deed reconveying the property to the borrower. You can find a Deed of Full Reconveyance on the Find A Form page of our website.

For more Information

At the law library:.

Deeds for California Real Estate KFC 170 .R36 (Self Help)

The Deed of Trust must be in a format the Sacramento County Recorder’s Office will accept. See the sample templates of the Deed of Trust and the Promissory Note below.

This material is intended as general information only. Your case may have factors requiring different procedures or forms. The information and instructions are provided for use in the Sacramento County Superior Court. Please keep in mind that each court may have different requirements. If you need further assistance consult a lawyer.

- Contact Us: (916) 442-4204 Tap Here To Call Us

A Deed of Trust can be Assigned Apart from the Note, and that often occurs just before a foreclosure. But What Does That Mean? Not Much, the Deed of Trust is Inseparable from the Note

Notes and Deeds of Trust are often assigned to different parties. The question posed is what happens if the Deed of Trust alone is assigned ? A typical assignment of the Deed of Trust alone will purport to assign “all beneficial interest under that certain Deed of Trust dated xyz..” But the long-established law in California is clear: the beneficial interest under a Deed of Trust is held by the party who holds the Note (or is entitled to enforce it), without regard to the assignment of the Deed of Trust .

The subject was again addressed by the California Courts in Domarad v. Fisher & Burke, Inc. (1969) 270 Cal. App. 2d 543 ). The Court noted that a deed of trust is a mere incident of the debt it secures and that an assignment of the debt carries with it the security. “The deed of trust is inseparable from the debt and always abides with the debt, and it has no market or ascertainable value, apart from the obligation it secures and that a deed of trust has no assignable quality independent of the debt, it may not be assigned or transferred apart from the debt, and an attempt to assign the deed of trust without a transfer of the debt is without effect. (emph. added)”

In Stockwell v. Barnum ((1908) 7 Cal. App. 413) the Court stated that this Code “is wholly foreign to deeds of trust, which, instead of creating a lien only, as in the case of a mortgage, passes the legal title to the trustee, thus enabling him in executing the trust to transfer to the purchaser a marketable record title. It is immaterial who holds the note. The transferee of a negotiable promissory note, payment of which is secured by a deed of trust whereby the title to the property and power of sale in case of default is vested in a third party as trustee, is not an incumbrancer to whom power of sale is given…” Stockwell @ 417.

And more recently “it has been established since 1908 that this statutory requirement that an assignment of the beneficial interest in a debt secured by real property must be recorded in order for the assignee to exercise the power of sale applies only to a mortgage and not to a deed of trust.” ( Calvo v. HSBC Bank USA, N.A. (2011) 199 Cal.App.4th 118 , 122.)

Why is that? There is a technical difference between the two security instruments. The mortgage only involves two parties –the borrower who grants the power of sale to the lender, and the lender who then holds the beneficial interest in the mortgage plus the power of sale. A deed of trust, on the other hand, involves three parties: the borrower, the lender, and the trustee who is granted conditional title to the encumbered property as well as the power of sale.

Thus, the deed of trust may thus be assigned one or multiple times over the life of the loan it secures. But if the borrower defaults on the loan, only the current beneficiary may direct the trustee to undertake the nonjudicial foreclosure process. “[O]nly the ‘true owner’ or ‘beneficial holder’ of a Deed of Trust can bring to completion a nonjudicial foreclosure under California law.” Yvanova v. New Century Mortgage (62 Cal. 4th 919) (2016)

An Alternative The Commercial Code also provides a mechanism for recording an assignment of the security if there has been an off-record transfer of the note but no recorded assignment of the deed of trust or mortgage. The buyer of the note can record a copy of the transfer agreement whereby the note was acquired, together with a sworn statement that a default has occurred, and in that event may proceed with a nonjudicial foreclosure. ( Cal. Com. Code, § 9607, subd. (b))

Photos: flickr.com/photos/discoveroregon/49807993897/sizes/l/ flickr.com/photos/mlp52/5208316490/sizes/l/ flickr.com/photos/hazphotos/2615058018/sizes/c/

Assignment of Deed

Table of contents, assignment of deed of trust.

An assignment of deed is used to show the deed of a property changing from one party to another, such as when a sale is made. It is used as the written proof to show who has rightful ownership of the property. When someone is purchasing property and decides to sell it before they have paid it off, an assignment of deed form would be used to transfer the rights and everything associated with the property over to the new owner.

When a debtor transfers real estate to a creditor, the Assignment of Deed is the legal document used to record this transfer. This happens when a lawsuit is filed on a property owner for a default in payment and the court’s rule in favor of the creditor; this is one example of when the deed of assignment would be put in to use. It’s used to show that the property is being transferred from the ownership of the defendant and given to the plaintiff that won the case and awarded the property.

It’s important to understand what these documents mean as they pertain to public property records as well as personal background checks into an individual. This could be exactly the type of information you need to help you gain a better understanding on someone or his or her history. It could also be in your own public background information if someone knows where to look for it.

Public records will always contain the history of who owns real property and the details on that property as it exchanges hands or ownership is passed. Anyone who knows how can access basic information about a deed or its assignments.

When a property owner uses an assignment of deed of trust, they are assigning ownership of the property to someone else and this is a very important document that should be kept in a safe and secure place. There are also public records kept on these types of documents and you should be able to request a copy – sometimes at a fee – should you need one.

The Assignment of Deed will also specify the rights the other person will receive along with the deed. As property transfers ownership like this, a recital is usually included as well which shows how many people and the identities of who has owned the property before. This allows you to see how many times the property has transferred hands over the course of its history.

Now that you know more about this particular property document, you will understand it when you use it. Whether you need it for your property or you are searching the property records of someone else for some reason, this information will be very beneficial to you.

We know that these types of legal matters can be confusing to the average person and that’s why we strive to make it easier to understand by giving you the basics here. Assignment of deed of trust documents do not have to confuse you anymore.

Assignment of Deed of Trust (Commercial Real Estate Loan) (TX) | Practical Law

Assignment of Deed of Trust (Commercial Real Estate Loan) (TX)

Practical law standard document w-035-0853 (approx. 18 pages).

MANAGING YOUR MONEY

2022 tax center.

- Share It Share Tweet Post Email Print

What Is a Deed of Trust With Assignment of Rents?

6 Tips to Save Using the Most Popular Food Delivery Apps

Some states refer to a voluntary lien against real property in exchange for money as a mortgage, while others refer to it as a deed of trust. Both mortgages and deeds of trust may incorporate an assignment of rents and leases that allows the lender to collect rent money held by,or due to, the property owner by tenants once the owner defaults or fails to make payments. An assignment of rents and leases may also be recorded as a separate document.

Absolute Assignment

A lender may require a borrower to execute an absolute assignment of rents in conjunction with a deed of trust. This conveys the rents to the lender at the time of the assignment but, in actuality, allows the borrower, as a licensee, to continue to collect the rents so long as the deed of trust is not in default. Payments under an absolute assignment will ordinarily be paid to the borrower or owner of the property as long as the loan secured by the deed of trust is not in default.

Collateral Assignment

In a collateral assignment, the borrower is generally considered to retain ownership of the rents until the lender takes action to enforce the assignment or gains possession of the property through foreclosure. One concern for the lender in this instance is that, in a judgement, other creditors will take priority, causing the lender to lose its security interest in the rent.

Rights After Default

Under an absolute assignment, if a borrower defaults on the deed of trust, the lender may request appointment of a receiver to collect the rents until foreclosure of the deed of trust or a determination of ownership of rents by a court of law. This prevents the borrower’s disposing of rent money due the lender, pending foreclosure. Under a collateral interest, however, some bankruptcy courts have held that the rents belong to the borrower until title to the real estate merges with the right to collect rents. If this is the case, and the borrower continues to operate as a debtor-in-possession of the property under bankruptcy, the lender may not be entitled to receive any rent money unless or until the bankruptcy court allows foreclosure of the property.

Uniform Assignment of Rents Act

Due to the inconsistency in interpretation of state law pertaining to assignment of rents and leases, some states have adopted a Uniform Assignment of Rents Act that better clarifies how rent monies will be handled in the event of default under the deed of trust and loan documents. The uniform act generally strengthens the lender’s position by recognizing his interest in rent money pending foreclosure and bankruptcy proceedings.

- Agentxtra.net: Assignment of Rents, Leases and Profits

- Polsinelli Shughart: Exercising an Assignment of Rents: Who is Entitled to the Money?

- Andrews Kurth, LLP: Texas Enacts the Texas Assignment of Rents Act

- Much Shelist: Assignment of Rents in Illinois: Shaky Ground for Commercial Lenders

Marie Murdock has been employed in the legal and title insurance industries for over 25 years. Murdock was first published in print in 1979 and has been writing online articles since mid-2010. Her articles have appeared on LegalZoom and various other websites.

Create your Deed of Trust and Assignment (for shares of stock) in minutes.

Step-by-step assistance.

Click the "Begin Here" button at the top of this page to start creating your document. Answer questions and download your customized document once finished.

Look for the following icons as you answer the Q&A to know more about the question and our suggested answer.

What is this?

Click this icon for information about the question.

Suggested Answer

Click this icon to know what is the recommended answer based on similar documents.

Things you need to know about Deed of Trust and Assignment (for shares of stock).

1. what is a deed of trust and assignment.

In a Deed of Trust and Assignment, the signor (the trustee) confirms that he/she is holding certain shares of stock in a corporation only in trust for the benefit of another person (the trustor).

The signor also appoints the Corporate Secretary of the corporation that issued the shares of stock as his/her attorney-in-fact to sell, assign and transfer the shares of stock in favor of the trustor or any person designated by the trustor.

2. What information do you need to create the Deed of Trust and Assignment?

To create your Deed of Trust and Assignment, you’ll need the following minimum information:

- The name and details (i.e. nationality and address) of the trustee

- The name of the trustor

- The number of shares held in trust

- The corporation which issued the shares of stock

3. How much is the document?

The document costs PhP 350 for a one-time purchase.

You can also avail of Premium subscription at PhP 1,000 and get (a) unlimited use of our growing library of documents, from affidavits to contracts; and (b) unlimited use of our “ Ask an Attorney ” service which lets you consult an expert lawyer anytime for any legal concern you have.

Document Name

Cancel Save

9 Eymard Drive, New Manila Quezon City Owned and operated by JCArteche’s Online Documentation & Referral Services

Back to Top

- Terms of Service

- Privacy Policy

- Create Documents

- Ask An Attorney

- How It Works

- Customer Support

IMAGES

VIDEO

COMMENTS

Download Or Email Form 1158 & More Fillable Forms, Register and Subscribe Now! pdfFiller allows users to Edit, Sign, Fill & Share all type of documents online. Try Out!

Assignment. When a lender sells the loan, it assigns the trust deed to the buyer. "Assignment" means to convey a claim or a right to another party, known as the "assignee.". This is done by creating another legal document — the assignment of trust deed — and having it signed by both buyer and seller. The trust deed, and other ...

An assignment of trust deed is necessary if a lender sells a loan secured by a trust deed. It assigns the trust deed to whoever buys the loan (such as another lender), granting them all the rights ...

A deed of trust is similar to a mortgage, and like a mortgage, it may include an assignment of rents. An assignment of rents gives the lender the right to step in and collect rent from the tenants if the borrower defaults on the loan payments. This right is absolute in some states but not in others.

A deed of trust is a real estate transaction agreement that allows a third-party trustee to hold the property title until the borrower repays the lender in full. The third party in a deed of trust ...

Assigning Trust Deeds. For financial benefit, lenders sometimes choose to sell their rights in deed of trust mortgages to other lenders. This process is known as assignment of the mortgage.

To transfer ownership rights in real estate, a grant deed is commonly used. When a loan is obtained to purchase real estate, a deed of trust is often used to give the lender rights in the real ...

Deeds of trust are used in conjunction with promissory notes. The deed of trust is the security for the amount loaned to finance the real estate purchase, and is secured by the underlying piece of real estate. The deed of trust is what secures the promissory note. The promissory note includes the interest rate, the payment amounts and terms ...

Deed of Trust Example Concerning an Assignment of Deed of Trust. An example of a deed of trust action can be found in the case of Maria Mendoza v JPMorgan Chase Bank. In November of 2007, Maria and Juan Mendoza took out a loan in the amount of $540,600 from JPMorgan Chase Bank. The loan was secured by a deed of trust.

A deed of trust (also known as a trust deed) is a document sometimes used in financed real estate transactions, generally instead of a mortgage. Deeds of trust transfer the legal title of a ...

Trust Deed: A trust deed is a notice of the release of merchandise to a buyer from a bank, with the bank retaining the ownership title to the released assets. The bank remains the owner of the ...

Again, while a mortgage involves two parties, a deed of trust involves three: the trustor (the borrower) the lender (sometimes called a "beneficiary"), and. the trustee. The trustee is an independent third party, like a title company, trustee company, or bank. The trustee holds "bare" or "legal" title to the property.

A trust deed is always used together with a promissory note (also called "prom note") that sets out the amount and terms of the loan. The property owner signs the note, which is a written promise to repay the borrowed money. A trust deed gives the third-party "trustee" (usually a title company or real estate broker) legal ownership of ...

A typical assignment of the Deed of Trust alone will purport to assign "all beneficial interest under that certain Deed of Trust dated xyz.." But the long-established law in California is clear: the beneficial interest under a Deed of Trust is held by the party who holds the Note (or is entitled to enforce it), without regard to the ...

An assignment transfers all the original mortgagee's interest under the mortgage or deed of trust to the new bank. Generally, the mortgage or deed of trust is recorded shortly after the mortgagors sign it, and, if the mortgage is subsequently transferred, each assignment is recorded in the county land records.

A short form deed of trust useful for commercial loans secured primarily by real estate. This Standard Document assumes an accompanying loan agreement contains the business terms, including provisions setting out the events of default and lender's rights and remedies. This Standard Document is useful in states that use deeds of trust, rather than mortgages, as the customary security instrument ...

Assignment of Deed of Trust. When a property owner uses an assignment of deed of trust, they are assigning ownership of the property to someone else and this is a very important document that should be kept in a safe and secure place. There are also public records kept on these types of documents and you should be able to request a copy ...

An assignment of deed of trust under Texas law. This Standard Document can be used to assign and transfer the beneficial interest under a Texas deed of trust from one lender to another lender. This Standard Document is intended for use with the financing of commercial properties in Texas and has integrated notes with important explanations and drafting and negotiating tips for both the ...

Under an absolute assignment, if a borrower defaults on the deed of trust, the lender may request appointment of a receiver to collect the rents until foreclosure of the deed of trust or a determination of ownership of rents by a court of law. This prevents the borrower's disposing of rent money due the lender, pending foreclosure.

A deed of trust with assignment of rents acts as extra security for the lender. It gives the lender the right to collect any rents that the property generates if you don't make your loan payments. The lender records a notice of default against you and can then can present a copy of the notice along with a copy of the deed of trust with ...

FOR VALUE RECEIVED, the undersigned hereby grants, assigns and transfers to. all beneficial interest under that certain Deed of Trust dated executed by. to and recorded as Instrument No. Recorder's office of. on. , as Trustor , Trustee , of Official Records in the County County, California. Describing land therein as (insert legal description):

SHORT FORM DEED OF TRUST AND ASSIGNMENT OF RENTS. ORDER NO. The following is a copy of provisions (1) to (14), inclusive, of the fictitious deed of trust, recorded in each county in Cal ifornia, as stated in the foregoing Deed of Trust and incorporated by reference in said Deed of Trust as being a part thereof as if set forth at length therein.

The document costs PhP 350 for a one-time purchase. You can also avail of Premium subscription at PhP 1,000 and get (a) unlimited use of our growing library of documents, from affidavits to contracts; and (b) unlimited use of our " Ask an Attorney " service which lets you consult an expert lawyer anytime for any legal concern you have.

Declaration of Trust and Deed of Assignment Sample - Free download as Word Doc (.doc), PDF File (.pdf), Text File (.txt) or read online for free. Draft Declaration of Trust of Shares

Assignment of Deed of Trust, Amended Deed of Trust, Abstract of Judgment, Affidavit, Assignment of Rents, Assignment of Lease, ... Uniform Commercial Code Amendment, Assignment, Continuation, Statement, or Termination 1-2 pages 3 or more pages *UCC's subject to Building Homes and Job Acts, Real Estate Fraud Fees, AB1466