A step-by-step guide to build a personal financial plan

Create a unique-to-you, start-to-finish plan for all your money goals with tools and resources to help you succeed.

When it comes to life's biggest moments, you probably had a plan. Your wedding, for example, followed a timeline, a budget—even if you busted it with that last-minute table for extended family—and involved compromise and conversation. Smart financial planning follows the same logic.

Our how-to articles (linked below) can help. They take you step-by-step through what you need to know to create a personal financial plan and help get your money in order. From the groceries you need, to the retirement you want, and the car repair bill that’s looming, these ideas help you balance long-term dreams with short-term wants, plus those unexpected events that happen along the way.

In nine steps, you have a nice framework you can build on and adjust throughout your life.

It’s OK if you’ve started on some of these tasks. It’s also OK if you haven’t. Just start with one and keep going. (Or tackle the whole thing on a long, rainy weekend with a big pot of coffee and the dog at your feet.)

Let’s get started.

1. Set financial goals.

It’s good to have a clear idea of why you’re saving your hard-earned money. Think it through with a five-step guide to setting yearly financial goals (worksheet included).

2. Make a budget.

Instead of thinking of a budget as way to restrict your spending, use it as a tool to organize your monthly cash flow to help you pay yourself first (savings/investing)—and still have room for the fun stuff. Learn how to create a budget that works for you—not against you. (Downloadable budgeting sheet included.)

3. Plan for taxes.

It can go a long way toward helping you keep more of your money. Explore ways to save on your taxes next year , using our tax planning worksheet to think through potential income tax credits and deductions.

4. Build an emergency fund.

All the planning in the world won’t help if life throws you a curveball and you’re not prepared financially. That’s where emergency savings comes in handy. Our guide to building an emergency fund includes to a calculator to help you figure out how much you need to save and teaches you how to maintain it over time.

5. Manage debt.

Understanding and managing debt is a key part of creating a financial plan. Learn how to pay off the debt you owe now and build a long-term debt-management strategy (worksheet and calculator included).

6. Protect with insurance.

Life can change in an instant. People with a good financial plan hope for the best, but plan for the unexpected. Insurance helps with that. Learn the basics of life and disability insurance (and use our disability income calculator to assess your needs).

7. Plan for retirement.

Even if it’s a long way off, think about what you want your money to do for you when you retire, and create a retirement plan to help make it happen.

8. Invest beyond your 401(k).

To reach your mid- and long-term goals, take your savings strategy and put an engine behind it. That’s what investing can do. Get started in three steps .

9. Create an estate plan.

You don’t have to be wealthy, old, married, or a parent to need an estate plan, which also lays out who makes financial and health care decisions for you if you can’t make them yourself. Learn the basics of estate planning and options for creating one.

Finished? Here’s when to review your financial plan.

Take a fresh look at least once a year or after a big life change, such as:

- Significant change in income

- Change in family dynamics like having a baby or adopting, getting married, divorced, or losing a spouse/partner

- Selling or buying a home

- Inheritance

- Unexpected debt

- Change in financial goals

Tip: Around age 50, you may want to consider long-term care insurance and expand your financial plan to include income in retirement.

What’s next?

Log in to your Principal account to see how you’re doing. Don’t have an employer-sponsored retirement account or want to save even more in addition to a 401(k)? We can help you set up your own IRA or Roth IRA . Ready to continue building your financial foundation?

Finance 101: What is credit, a credit score, and a credit report (and why they matter)

Understand the factors that make up a credit score and know how to check your credit report to help build your financial foundation.

What’s investment risk and risk tolerance (and how to navigate them both)

Risk accompanies all sorts of activities, including investment. What types of risks may impact your retirement and savings accounts?

What are the options for your pension payout?

Comparing the choices for your defined benefit/pension payout may help you figure out how to reach your retirement goals.

The subject matter in this communication is educational only and provided with the understanding that Principal ® is not rendering legal, accounting, investment advice or tax advice. You should consult with appropriate counsel or other advisors on all matters pertaining to legal, tax, investment or accounting obligations and requirements.

How to Create a Personal Financial Plan (And Reach Your Goals Faster)

We all have goals in life – things like starting a business , buying a house, getting married – but money problems often sneak in and prevent us from achieving these objectives.

And so we are left wishing we had done some financial planning to pay for the necessities and to cover any of life’s unexpected events … and we’d still have enough left to put towards our goals.

If any of this sounds familiar to you, then you probably don’t have a financial plan in place.

At its most basic, a financial plan helps you meet your current financial needs and offers a strategy to achieve future financial stability, so you’re able to move forward with your goals.

In this post, you’ll learn everything you need to know about financial plans. We’ll also share an eight-step process to help you create your own personal financial plan, plus a few templates that can help you save money and time.

Post Contents

What is a Financial Plan?

What is a personal financial plan, step 1: review your current situation, step 2: set short-term and long-term goals, step 3: create a plan for your debts, step 4: establish your emergency fund, step 5: start estate planning, step 6: begin investing in your future, step 7: get protected, step 8: keep track of your plan, daily successful living’s financial plan template, smartsheet’s one-page financial plan template, simply stacie’s printable financial planner, financial plan app options, want to learn more.

Start selling online now with Shopify

A financial plan is a roadmap for an individual or a company to reach its goals.

It takes into your account your existing financial situation and goals, then creates a detailed strategy based on your prioritized objectives, telling you exactly where to spend your money, and when to save.

→ Click Here to Launch Your Online Business with Shopify

Additionally, financial plans help you prepare for the unanticipated by having you set aside a pot of money. When an unexpected job loss , illness or economic downturn occurs, you can rely on these funds to cover your day-to-day expenses.

Essentially, you can use a financial plan to take control of your money such that you can achieve your goals and ease worries you may have about your wellbeing.

In the past, people had to hire a professional to create a financial planner for them. But with the advancements in technology, you should be able to create one on your own.

It’s pretty easy with a financial plan template, which you can modify to reflect your own goals, cash flow, etc. You’ll find some handy templates you can use, later in the article.

A personal financial plan is a documented analysis of your personal finances, including your earnings, liabilities, assets, and investments.

Its purpose is to help you assess the feasibility of your personal goals and to understand the steps that you will need to take – money-wise – to accomplish them.

Your personal financial plan can stretch over weeks, months or years, based on the estimated completion time of your goals.And you can adjust it at any time to reflect new or changing priorities.

How to Create a Personal Financial Plan in 8 Easy Steps

Making a financial plan could give you more confidence with your cash. Plus, it means fewer nights worrying about those pesky bills.

The trouble is many people don’t know where to get started. They worry about things like “how much does a financial plan cost?” and assume they need endless professional support.

The good news? It’s never too late (or too early) to start working on your financial plan. Even better – creating a financial plan isn’t as complicated as you’d think. You can even break it down into 8 easy steps, like this:

Before you start the actual “planning” part of the process, you need to know where your journey is going to start. That means checking out what your financial situation is like right now.

Honestly, everyone could benefit from investing in more frequent financial checkups, but it’s easy to put off looking at your bank statements.

Think about it – when’s the last time you actually looked at all of your payments for gas, electricity, broadband, and Netflix, and figured out what they add up to?

Grab your last 6 to 12 months of bank statements and highlight every regular outgoing expense in one color, then highlight your irregular expenses in another.

It might be helpful to categorize these costs into personal and “crucial” expenses. Once you’ve got all the right info in front of you, ask yourself:

- Where can I cut down on spending?

- How much could I save by switching to a different service?

- Do I really need all of my “optional” expenses?

Now you have a starting point for your journey to financial freedom.

The next step is figuring out where you’re going. This is an important component in your “financial plan for dummies” journey.

Setting solid goals gives you direction and clarity when making decisions about your finances. Your goals will show you if you’re moving in the right direction.

Ideally, you’ll need your goals to be S.M.A.R.T. This means they’re:

Don’t just say you want to have more money in your savings. Write down a statement that explains exactly what you want to accomplish, such as:

“I want to have at least $2,000 in my savings account by the end of next year.”

Short-term financial goals, like “I’ll put $100 in my savings next month”, keep you motivated by showing constant progress. Long-term goals give you a more consistent direction to move in.

No-one likes thinking about debts – but these are issues that you just can’t ignore if you want to be financially savvy. Personal financial plans can help.

You can’t make huge progress with your short and long-term goals if your interest and repayments are weighing you down. So figure out how to pay what you owe first.

Start by creating a plan to get rid of your most problematic debts. These are the expenses that cost the most due to excessive interest rates and fees. Get rid of those as fast as you can.

If you’re struggling to handle several debts at once, it might help to see whether you can consolidate everything into one, cheaper loan.

The bottom line is you need to take action and start working towards being debt-free. Remember, debts include everything from immediate issues, like credit cards, to long-term expenses, like student debt .

An emergency fund is like a financial safety blanket.

No matter how “prepared” you think you are, there’s always a chance that some unexpected cost will come and sweep you off your feet.

Emergency funds protect you against things like unexpected illness, suddenly losing your job, or even just a bill that you forgot to pay.

While the exact amount of emergency funding you have depends on you, it should generally cover about 3 to 6 months’ worth of your fixed expenses. You can also save enough to cover variable expenses like entertainment and food too.

Emergency funds are beneficial for anyone. However, they’re particularly important if you’re a freelancer , someone with a poor credit score, or someone with variable income.

When setting up your personal financial plans, make sure you have an emergency fund in place.

Estate planning is one of those complicated terms that most people ignore – assuming it only applies to wealthy people, or people approaching retirement .

However, it’s essential that you think about protecting your family when you’re not around. A proper estate plan gives you total peace of mind.

Estate plans include:

- Last will and testament

- Healthcare directives

- Power of attorney

- Trust information

This document might also include other clauses for things like final disposition instructions and guardianship nominations.

Estate planning might not be the best thing you can do with your Friday evening fun-wise, but it will ensure that you’re protected for anything.

The next step is building whatever wealth you already have, so you’re prepared for the future. You can begin focusing on your savings and making investments.

You might have different plans to suit your short-term and long-term goals. For instance, your short-term financial plan might cover the steps you’re going to take to build wealth now. Your 5-year financial plan might look at things like retirement.

Investing for retirement is one of the best ways to ensure that you’re ready to tackle the future. When you begin planning for retirement, you’ll need to consider a few variables like:

- Desired retirement age: When would you like to stop working (be realistic here)

- Desired lifestyle: What kind of lifestyle do you want? Do you want enough cash to do whatever you like? Then plan for that!

- Current health: Health is definitely a big contributor to wealth. If you know health problems are likely for you, make sure you’re ready to tackle the issue.

- Savings rate: How much are you saving towards the future right now?

If you’re brand-new to investing, seek out some extra support. There are wealth advisors out there that can introduce you to different kinds of investment accounts and vehicles.

Just as emergency funds protect you from unexpected surprises in life, insurance defends your cash from any unforeseen risks.

Having the right insurance means that you won’t need to constantly break into your savings every time something goes wrong. For instance, home insurance means that you’re properly protected from things like natural disasters and break-ins.

Car insurance ensures that if anything goes wrong with your car, you’re ready to jump in and fix the issue – without massive payments.

Having an emergency fund and making sure you’re insured properly means that you can stay on top of all your savings goals – even when the going gets tough.

Make a list of all the insurance you might need when planning financial plan components.

The importance of a financial plan is something you can’t afford to underestimate.

The more you know about your current financial situation and where you’re headed, the more confident you’ll be in your spending.

However, getting a financial plan example template and building your own strategy is just the first leg of the journey. You also need to commit to actively tracking your progress.

Check in every three months or so, and make sure you’re moving in the right direction. A lot can change in your financial situation within just a few weeks.

Remember to update your plan when significant events occur in your life too. Having a child, getting married, or purchasing a new home will all create new considerations for you to deal with.

Actively reviewing and updating your plan means that you can enjoy a bullet-proof strategy for reaching your financial goals.

Financial Plan Example [Templates]

While you can create a financial plan from scratch, it’s always easier and quicker with a template.

Many financial plan template options are available to help you set up a financial plan. All you need to do is enter the details in their fields. You can also edit or remove fields based on the information you have available.

Even if you don’t want to use templates, these financial plan examples are a good starting point to learn what real-world plans look like and the specific finances you have to include in the document.

Here are a few templates:

Daily Successful Living offers a simple template you can use to calculate your net worth.

You can do this by adding up your assets and then subtracting all of your liabilities.

Once you have estimated your net worth, you can move onto setting some personal goals.

Smartsheet’s free financial plan template lets you create a concise personal finance plan.

Use it to assess your current financial situation, create a strategy to reach your goals, and use the plan to track progress.

You can also include details for estate planning or life insurance if needed.

Simply Stacie’s financial planner allows you to lay it all out – month-to-month – to analyze your monthly spending habits compared to what you budgeted.

If you’re working towards a goal like, say, saving for retirement, it’ll help you find opportunities to cut back and put the money towards your objective.

Keeping track of your money is difficult, especially when you’re unsure of your spending.

Fortunately, there are budget apps you can use to stay on top of your finances.

- Mint : Mint, besides its pleasingly minimal UI, offers a good range of money management tools. These are set around a few different areas, namely expense tracking, credit health, and saving advice tailored to your goals.

- Pocketnest : Pocketnest teams up with your bank to take you through different themes of financial planning. After you answer a few questions about your financial hitch, the app walks you through each stage of your plan, giving you to-dos along the way to help address any gaps.

- YNAB : YNAB offers bank syncing, transaction matching, goal tracking, and more. It can help you prepare for the future by breaking up larger expenses into more manageable, bite-sized amounts. The best expenses are ones you can easily manage.

Each of these apps make creating a financial plan a lot more convenient. Being able to view your income, expenditures, investments, etc. at a glance helps you jot down details much faster than gathering information from individual accounts.

Financial plans aren’t just for people with high income. Anyone can utilize them to identify their goals and create a plan for achieving them.

If you create a financial plan today, you would be able to work on achieving your life’s goals strategically.

It doesn’t matter where you stand. The important thing is that you get to fulfill your ambitions while improving your financial stability.

Do you want to start a side hustle , go on a holiday, retire by 40? You decide and then create a personal financial plan for achieving your purpose.

P.S. Life’s going to throw you curveballs that can affect your financial situation. Rather than accepting them as your fate, battle through them. You have the most powerful weapon of them all – your financial plan!

- 10-Step Formula to Achieve Financial Freedom in 2021

- 30 Personal Finance Tips You Need to Know

- Money Blogs: The Best Personal Finance Blogs in 2021

- Economic Recession: What Steps Can You Take Now?

Oberlo uses cookies to provide necessary site functionality and improve your experience. By using our website, you agree to our privacy policy.

- CRM Asignment Help

- MBA Assignment Help

- Statistics Assignment Help

- Market Analysis Assignment Help

- Business Development Assignment Help

- 4p of Marketing Assignment Help

- Pricing Strategy Assignment Help

- Operations Management Assignment Help

- Corporate Strategy Assignment Help

- Change Management Assignment Help

- Supply Chain Management Assignment Help

- Human Resource Assignment Help

- Management Assignment Help

- Marketing Assignment Help

- Strategy Assignment Help

- Operation Assignment Help

- Marketing Research Assignment Help

- Strategic Marketing Assignment Help

- Project Management Assignment Help

- Strategic Management Assignment Help

- Marketing Management Assignment Help

- Business Assignment Help

- Business Ethics Assignment Help

- Consumer Behavior Assignment Help

- Conflict Management Assignment Help

- Business Statistics Assignment Help

- Managerial Economics Assignment Help

- Project Risk Management Assignment Help

- Nursing Assignment Help

- Clinical Reasoning Cycle

- Nursing Resume Writing

- Medical Assignment Help

- Financial Accounting Assignment Help

- Financial Services Assignment Help

- Finance Planning Assignment Help

- Finance Assignment Help

- Forex Assignment Help

- Behavioral Finance Assignment Help

- Personal Finance Assignment Help

- Capital Budgeting Assignment Help

- Corporate Finance Planning Assignment Help

- Financial Statement Analysis Assignment Help

- Accounting Assignment Help

- Solve My Accounting Paper

- Taxation Assignment Help

- Cost Accounting Assignment Help

- Managerial Accounting Assignment Help

- Business Accounting Assignment Help

- Activity-Based Accounting Assignment Help

- Economics Assignment Help

- Microeconomics Assignment Help

- Econometrics Assignment Help

- IT Management Assignment Help

- Robotics Assignment Help

- Business Intelligence Assignment Help

- Information Technology Assignment Help

- Database Assignment Help

- Data Mining Assignment Help

- Data Structure Assignment Help

- Computer Network Assignment Help

- Operating System Assignment Help

- Data Flow Diagram Assignment Help

- UML Diagram Assignment Help

- Solidworks Assignment Help

- Cookery Assignment Help

- R Studio Assignment Help

- Law Assignment Help

- Law Assignment Sample

- Criminology Assignment Help

- Taxation Law Assignment Help

- Constitutional Law Assignment Help

- Business Law Assignment Help

- Consumer Law Assignment Help

- Employment Law Assignment Help

- Commercial Law Assignment Help

- Criminal Law Assignment Help

- Environmental Law Assignment Help

- Contract Law Assignment Help

- Company Law Assignment Help

- Corp. Governance Law Assignment Help

- Science Assignment Help

- Physics Assignment Help

- Chemistry Assignment Help

- Sports Science Assignment Help

- Chemical Engineering Assignment Help

- Biology Assignment Help

- Bioinformatics Assignment Help

- Biochemistry Assignment Help

- Biotechnology Assignment Help

- Anthropology Assignment Help

- Paleontology Assignment Help

- Engineering Assignment Help

- Autocad Assignment Help

- Mechanical Assignment Help

- Fluid Mechanics Assignment Help

- Civil Engineering Assignment Help

- Electrical Engineering Assignment Help

- Ansys Assignment Help

- Humanities Assignment Help

- Sociology Assignment Help

- Philosophy Assignment Help

- English Assignment Help

- Geography Assignment Help

- History Assignment Help

- Agroecology Assignment Help

- Psychology Assignment Help

- Social Science Assignment Help

- Public Relations Assignment Help

- Political Science Assignment Help

- Mass Communication Assignment Help

- Auditing Assignment Help

- Dissertation Writing Help

- Sociology Dissertation Help

- Marketing Dissertation Help

- Biology Dissertation Help

- Nursing Dissertation Help

- MATLAB Dissertation Help

- Law Dissertation Help

- Geography Dissertation Help

- English Dissertation Help

- Architecture Dissertation Help

- Doctoral Dissertation Help

- Dissertation Statistics Help

- Academic Dissertation Help

- Cheap Dissertation Help

- Dissertation Help Online

- Dissertation Proofreading Services

- Do My Dissertation

- Business Report Writing

- Programming Assignment Help

- Java Programming Assignment Help

- C Programming Assignment Help

- PHP Assignment Help

- Python Assignment Help

- Perl Assignment Help

- SAS Assignment Help

- Web Designing Assignment Help

- Android App Assignment Help

- JavaScript Assignment Help

- Linux Assignment Help

- Mathematics Assignment Help

- Geometry Assignment Help

- Arithmetic Assignment Help

- Trigonometry Assignment Help

- Calculus Assignment Help

- Arts Architecture Assignment Help

- Arts Assignment Help

- Case Study Assignment Help

- History Case Study

- Case Study Writing Services

- Write My Case Study For Me

- Business Law Case Study

- Civil Law Case Study Help

- Marketing Case Study Help

- Nursing Case Study Help

- ZARA Case Study

- Amazon Case Study

- Apple Case Study

- Coursework Assignment Help

- Finance Coursework Help

- Coursework Writing Services

- Marketing Coursework Help

- Maths Coursework Help

- Chemistry Coursework Help

- English Coursework Help

- Do My Coursework

- Custom Coursework Writing Service

- Thesis Writing Help

- Thesis Help Online

- Write my thesis for me

- CDR Writing Services

- CDR Engineers Australia

- CDR Report Writers

- Homework help

- Algebra Homework Help

- Psychology Homework Help

- Statistics Homework Help

- English Homework Help

- CPM homework help

- Do My Homework For Me

- Online Exam Help

- Pay Someone to Do My Homework

- Do My Math Homework

- Macroeconomics Homework Help

- Jiskha Homework Help

- Research Paper Help

- Edit my paper

- Research Paper Writing Service

- Write My Paper For Me

- Buy Term Papers Online

- Buy College Papers

- Paper Writing Services

- Research Proposal Help

- Proofread My Paper

- Report Writing Help

- Story Writing Help

- Grant Writing Help

- DCU Assignment Cover Sheet Help Ireland

- CHCDIV001 Assessment Answers

- BSBWOR203 Assessment Answers

- CHC33015 Assessment Answers

- CHCCCS015 Assessment Answers

- CHCECE018 Assessment Answers

- CHCLEG001 Assessment Answers

- CHCPRP001 Assessment Answers

- CHCPRT001 Assessment Answers

- HLTAAP001 Assessment Answers

- HLTINF001 Assessment Answers

- HLTWHS001 Assessment Answers

- SITXCOM005 Assessment Answers

- SITXFSA001 Assessment Answers

- BSBMED301 Assessment Answers

- BSBWOR502 Assessment Answers

- CHCAGE001 Assessment Answers

- CHCCCS011 Assessment Answers

- CHCCOM003 Assessment Answers

- CHCCOM005 Assessment Answers

- CHCDIV002 Assessment Answers

- CHCECE001 Assessment Answers

- CHCECE017 Assessment Answers

- CHCECE023 Assessment Answers

- CHCPRP003 Assessment Answers

- HLTWHS003 Assessment Answers

- SITXWHS001 Assessment Answers

- BSBCMM401 Assessment Answers

- BSBDIV501 Assessment Answers

- BSBSUS401 Assessment Answers

- BSBWOR501 Assessment Answers

- CHCAGE005 Assessment Answers

- CHCDIS002 Assessment Answers

- CHCECE002 Assessment Answers

- CHCECE007 Assessment Answers

- CHCECE025 Assessment Answers

- CHCECE026 Assessment Answers

- CHCLEG003 Assessment Answers

- HLTAID003 Assessment Answers

- SITXHRM002 Assessment Answers

- Elevator Speech

- Maid Of Honor Speech

- Problem Solutions Speech

- Award Presentation Speech

- Tropicana Speech Topics

- Write My Assignment

- Personal Statement Writing

- Narrative Writing help

- Academic Writing Service

- Resume Writing Services

- Assignment Writing Tips

- Writing Assignment for University

- Custom Assignment Writing Service

- Assignment Provider

- Assignment Assistance

- Solve My Assignment

- Pay For Assignment Help

- Assignment Help Online

- HND Assignment Help

- SPSS Assignment Help

- Buy Assignments Online

- Assignment Paper Help

- Assignment Cover Page

- Urgent Assignment Help

- Perdisco Assignment Help

- Make My Assignment

- College Assignment Help

- Get Assignment Help

- Cheap Assignment Help

- Assignment Help Tutors

- TAFE Assignment Help

- Study Help Online

- Do My Assignment

- Do Assignment For Me

- My Assignment Help

- All Assignment Help

- Academic Assignment Help

- Student Assignment Help

- University Assignment Help

- Instant Assignment Help

- Powerpoint Presentation Service

- Last Minute Assignment Help

- World No 1 Assignment Help Company

- Mentorship Assignment Help

- Legit Essay

- Essay Writing Services

- Essay Outline Help

- Descriptive Essay Help

- History Essay Help

- Research Essay Help

- English Essay Writing

- Literature Essay Help

- Essay Writer for Australia

- Online Custom Essay Help

- Essay Writing Help

- Custom Essay Help

- Essay Help Online

- Writing Essay Papers

- Essay Homework Help

- Professional Essay Writer

- Illustration Essay Help

- Scholarship Essay Help

- Need Help Writing Essay

- Plagiarism Free Essays

- Write My Essay

- Response Essay Writing Help

- Essay Assistance

- Essay Typer

- APA Reference Generator

- Harvard Reference Generator

- Vancouver Reference Generator

- Oscola Referencing Generator

- Deakin Referencing Generator

- Griffith Referencing Tool

- Turabian Citation Generator

- UTS Referencing Generator

- Swinburne Referencing Tool

- AGLC Referencing Generator

- AMA Referencing Generator

- MLA Referencing Generator

- CSE Citation Generator

- ASA Referencing

- Oxford Referencing Generator

- LaTrobe Referencing Tool

- ACS Citation Generator

- APSA Citation Generator

- Central Queensland University

- Holmes Institute

- Monash University

- Torrens University

- Victoria University

- Federation University

- Griffith University

- Deakin University

- Murdoch University

- The University of Sydney

- The London College

- Ulster University

- University of derby

- University of West London

- Bath Spa University

- University of Warwick

- Newcastle University

- Anglia Ruskin University

- University of Northampton

- The University of Manchester

- University of Michigan

- University of Chicago

- University of Pennsylvania

- Cornell University

- Georgia Institute of Technology

- National University

- University of Florida

- University of Minnesota

- Help University

- INTI International University

- Universiti Sains Malaysia

- Universiti Teknologi Malaysia

- University of Malaya

- ERC Institute

- Nanyang Technological University

- Singapore Institute of Management

- Singapore Institute of Technology

- United Kingdom

- Jobs near Deakin University

- Jobs Near CQUniversity

- Jobs Near La Trobe University

- Jobs Near Monash University

- Jobs Near Torrens University

- Jobs Near Cornell University

- Jobs Near National University

- Jobs Near University of Chicago

- Jobs Near University of Florida

- Jobs Near University of Michigan

- Jobs Near Bath Spa University

- Jobs Near Coventry University

- Jobs Near Newcastle University

- Jobs Near University of Bolton

- Jobs Near university of derby

- Search Assignments

- Connect Seniors

- Essay Rewriter

- Knowledge Series

- Conclusion Generator

- GPA Calculator

- Factoring Calculator

- Plagiarism Checker

- Word Page Counter

- Paraphrasing Tool

- Living Calculator

- Quadratic Equation

- Algebra Calculator

- Integral Calculator

- Chemical Balancer

- Equation Solver

- Fraction Calculator

- Slope Calculator

- Fisher Equation

- Summary Generator

- Essay Topic Generator

- Alphabetizer

- Case Converter

- Antiderivative Calculator

- Kinematics Calculator

- Truth Table Generator

- Financial Calculator

- Reflection calculator

- Projectile Motion Calculator

- Paper Checker

- Inverse Function Calculator

Financial Planning Assignment: Development Of A Client's Financial Plan

Task: Your task is to write a financial planning assignment addressing the following parts:

Part 1 The assignment is based on material covered in weeks 2 to 9, however will involve reviewing course materials for week 10 and 12. You will be required to complete a detailed file note (1500 words) as preparation for development of a client's financial plan (Statement of Advice).

- to provide an overview of the client's circumstances (including their current situation and goals, tables of financial position) and provide potential wealth creation, wealth protection (insurance) and lifestyle strategies that address these circumstances and goals,

- to provide a list of assumptions you are making; and

- prepare a list of questions for the clients where further information may be required prior to completing the SoA.

Summary of transcript Date to use for initial contact: 1 August 2020

Emily and Joel Stevens Emily and Joel realise that they are not getting anywhere financially. They have decided it is time to bite the bullet and get their finances in order. They believe that a first glance, their finances seem good, but there are a number of issues that need to be resolved.

Emily earns $81,000 p.a. Her employer contributes the 9.5% Super Guarantee. She has not been contributing herself and at age 41, her balance is around $125,000 – she is aware that this is not a good outcome.

Joel, age 45, earns $122,000, and like Emily he has not been putting any extra into his super. His current balance is $156,000. They would like to retire when Emily turns 60 and believe they will need $49,000 in today’s dollars to live on.

They have an emergency savings account of $25,000 earning 0.5%. They also have a share portfolio currently worth $250,000 and $150,000 as a margin loan. The interest rate is 8% and the portfolio earns 3.0%. They are uncertain about this investment and see the interest payments eating up all of the earnings. It is also of concern how to fund university costs for their children Lauren who is 10 and Michael who is 8.

Several years ago, they inherited a rental property valued at $450,000. It is now worth around $570,000 but is only returning 4% - which after associated fees and charges ($4,280 per year) is actually lower. They are not that happy with the property but would hold onto it if it was financially suitable.

However, with the shares and the property, they are wondering if they are burdening themselves unnecessarily. They find it all confusing, time consuming and seemingly not very rewarding. On top of it all, they have to pay their accountant $1,800 a year to sort it all out. On the whole, they feel they earn a lot of money and never have an extra dollar to their name.

Emily and Joel feel ‘exasperated’. And the expenses!

Aside from paying the deductible expenses, they find they are spending a lot of money, and their credit card balance seems to get bigger each month.

Their mortgage balance on their on their home is $235,000, they have thought of refinancing.

When asked to itemise their expenses, they provided the following calculations:

They estimate their credit card balance is around $55,000 at approximately 17.75%

As for personal insurance, neither have income protection or trauma cover. Emily has $34,000 in life and TPD in her super and Joel has $64,000 life and TPD. Emily cannot get higher cover in her fund as the cover is standard. Joel can purchase up to three (3) times his salary. They are concerned about their budget if personal insurance is needed.

Part 2 A successful client meeting involves preparation, well-honed interpersonal skills and adherence to compliance procedures. All of this may come naturally to some advisers. However, for most, conducting a successful fact finding meeting is a skill that will be acquired and developed over time.(1000 words)

- Discuss how to prepare for a successful fact finding meeting.

- Explain the legal basis for using a fact find document.

- Outline the elements of a successful fact finding meeting.

The Profile of Advisor and FSG As per the case considered in this financial planning assignment, Joel and Emily Stevens were significantly handed with the Financial Services Guide (FSG) version 10, andthe interview was conducted on 1 August 2020, where I was the Advisor Profile. In significantly provided them with a proper guide towards their financial issues and saving. Moreover, the Corporations Act and Section 961 was duly taken into effective consideration for this advice. Using these aspects, the FSG was duly explained to the couple.

The Overall Scope of Advice The Full Statement of Advice (SOA) tends to provide effective advice concerning the various ways through which there can be an effective creation of wealth, and the goals in the lifestyle can be met in a significant manner. Moreover, it also provides effective factors through which substantial protection towards the income, as well as the trauma, can be maintained among the clients who seek advice regarding their financial position. It allows the client to achieve prominent protection towards their finance as well as allows in creating wealth for future safety.

However, in this SOA, the overall analysis of the cash flow, as well as the interpretation using budgeting, has not been taken into consideration and are completely excluded from this part. Moreover, the planning concerning social security as the repayment of the loans and debt are also not evaluated in this SOA. Proper recommendations towards their expenses and the risk that they can face in the future concerning their financial position are stated in a significant manner.

The Present Situation of the Clients

- One of the most significant aspects that have been observed for the couple is that they are left with only 45,050 dollars after meeting with the total expenditure on an annual basis. It was determined that after their retirement, they would need to have at least $ 49,000, and with the current surplus, they would still be under a deficit of $ 3,950on an annual basis.

- To minimise the overall expenditures and manage the expenses so that they are able to save for the future.

- To keep safety for the children after their retirement from their service.

- To meet with the average need for dollar, which is $ 49,000 in order to live after retirement.

- To have a good amount of emergency funds after their service period.

- To recommend a proper investment method in order to increase the bank balance and secure the future.

- To have proper insurance for their health after their service of employment.

- They would have a proper investment by being a conservative investor and get no negative results.

- Steven’s are having large expenses as compared to their income.

- The higher expenses would affect their future savings and livelihood, along with the education of the children.

- The negative results will be identified after they have been retired, and the sum would be $ 10,030 in total.

- There isa lesser number of defensive assets, and the weightageis also less, which will affect their savings.

- The fixed interest, along with the availability of cash, is also considerably less for them.

- They should have a lower risk concerning their growth as well as the earning capacity.

- The Stevens is to purchase a house and invest in the government bond with their savings.

- They are not investing in any cash flow.

- They are selling the inherited rental house at 20 per cent over the current market value.

- The new house will be purchased at $600,000, and the remaining amount will be used for repaying the credit card dues and the 17.5 per cent interest due on it.

- They have a higher risk of investing in cash flow, and the investment will be made on government bonds only.

- They are to be recommended with effective investment options at priority from the very beginning.

- They will be renting the new property, and the earnings from it will be used to safeguard their future after retirement.

- Was buying the new house effective towards your future gaols of financial stability?

- Was the financial burden significantly reduced by selling the low value house?

- Was buying the new house by selling the old house and rational decision?

Wealth Creation & Lifestyle Recommendations – Outside Superannuation

- It is recommended to Steven’s that they should buy a government bond at a fixed rate so that after retirement, they can earn by renting the place.

- They should sell the rental property they currently own as it has a very low return of 4 per cent.

- The government bond within Australia is paying a fixed rate 2.5 per centfor a tenyears’ time period.

- The surplus they have after the expenses should be saved until the retirement period is being met.

- After maturity, they would have a substantial amount of savings in order to provide proper education and meet with their yearly requirement.

- Owning a house, which has a higher return rate, will provide better security for Steven’s.

- The chosen strategy will allow in maximising their savings

- The income from the government bond will also increase from this strategy

- The surplus for each month will be used.

- Unable to sell the bonds before selling.

The calculation for Buying New House Considering they are selling the inherited rental house at 20 per cent over the current value, they would have (570000+ (570000*20/100)) = 6,84,000. The new house will be purchased at $ 6,00,000 and the rest $ 84,000 would be used to repay the dues on the credit card as well as the 17.5% interest on the credit card.

- They Should Invest around 70 per cent of the funds of superannuation for a longer time period thirty per cent should be invested in funds that are diversified(Refer to Appendix 1).

- Moving into assets that are more defensive would allow them to minimise the risk of facing the market volatility and recession in the economy.

- Moreover, diversified funds are less risky as compared to shares, and the losses are set off when profit is earned by another sector in the country.

- The rate of interest is fixed for the bonds from the government and would allow them to take less risk as they have very fewer savings and are on their early and mid-forties.

- The diversified funds are more extensive and less risky as no one sector is being focused on specifically.

- The rate of return is quite low as compared to the earning from shares.

- There are quite small returns from the funds that are diversified.

- The availability of the invested fund during an emergency is not an option.

Emily and Joel Stevens have faced a huge amount of expenditure in the past years and are unable to save money due to some issues. Life insurance is recommended to Joel and Emily as they have children, which can be called as dependencies. The children will be the beneficiaries of the policy only after the death of Emily and Joel. This policy is highly recommended to them according to me as the fees of schools, colleges are hiking every year, and the cost of higher studies is more than expected.

The main advantage of this policy is that the children will be able to survive if anything happens to Emily and Joel.

However, the disadvantage is that Joel and Emily will not be able to get the benefits of the policy.

- Total and permanent disability provides an insurance policy that ensures the customers with disabilities policies, which may happen in case of any loss of legs or eyes or any physical challenges. This policy is applicable to the individuals that work in risky or dangerous places and have life risks.

- This policy cannot be recommended to Joel and Emily according to my views.

- One of the prime advantages of this policy is that the affect6ed get a massive sum of money if he/she is medically diagnosed with issues of inability to work.

- However, the disadvantage is that this policy is only applicable to the individuals that have suffered permanent and total disability in the work process.

- Income protection is a policy of insurance where the policyholder is obliged by the insurer specific facilities when he is unable to conduct his work in case of any illness or accident.

- I would recommend Joel and Emily to apply for this policy because they are seeking to protect their wealth and income, as they do not have much savings in their accounts even after earning a considerable amount of money.

- The advantage of this policy is that in case of any sickness that has happened to the children, they are able to gain benefits from this type of insurance.

- It also ensures the income of the policyholder if the person is not working due to some issues.

- Trauma insurance policy is also known as critical illness insurance that provides a massive sum of money to the policyholder to cover any emergency medical expenses.

- Financial needs are also covered up with this insurance in case of any critical injury or illness. I would recommend Emily and Joey this policy as they are getting old and may have any emergency issues in the future.

- There are many issues related to trauma, specifically intensive care or heart attacks, which are common these days, mostly in the middle age group. Such problems need a lump amount in healthcare, which is provided by this policy. This is the most crucial advantage of insurance.

- There is a disadvantage with this insurance that it can be only used in case of some serious illness like cancer or other life-threatening medical conditions

- Private health insurance is medical concealment applied if any policyholder is interested in taking private care at medical service. I would not like to recommend this to Emily and Joey as they need to save money at this point in time, and private services cost a huge sum of value.

- The advantages of this policy include admittance to private rooms, freedom of choice regarding doctors, and less time in getting services in the hospitals.

- The major disadvantage is that this policy is highly expensive and does not cover many factors of savings for the customers.

REFERENCES Chen, Z. and Sakouba, I., (2020). Impact of the number of bonds on bond portfolio exposure to interest rate risk. International Journal of Finance & Economics.

Appendix 1 – Calculation Of The Future Value Of Government Bond Evaluation of the Future value of Australian ten years government bonds that they will be investing in from their savings

Bond Rate of Australian 10 years government bond is 2.5%.

Consideringthat Stevens has $ 45,050(Total income minus expenses) to purchase bonds, the future value of bonds is given as follows:

Future Value =Present value* (1 + interest rate) ^Period

Amount = 45,050;

Interest rate = 2.5%

Period = 10 years government bond.

Future Value = 45,050* (1+0.025) ^10 = $57,664

Thus, they would be earning more than what was required for the future, which was $49,000 and by investing the 10 years Australian government bond, they would be earning $ 57,664.

CHECK THE PRICE FOR YOUR PROJECT

Number of pages/words you require, choose your assignment deadline, related samples.

- Financial Review assignment on Univeler PLC in a post Pandemic World

- Finance assignment depicting the ratio analysis of Nestle and Unilever and comparing which one is better than the other.

- Finance assignment using budgets and variance analysis for business planning

- Finance assignment evaluating the financial performance of MCDONALD for two consecutive years

- international finance assignment on the effect of Covid 19 on the major global economies

- (AF7006 / AF7011) Finance assignment a critical appreciation for strategic advantage for BHP and Rio Tinto

- Compliance with AASB Standards in JB Hi-Fi Limited Method of Depreciation: Improving Relevance and Authenticity of Financial Reports

- A finance assignment on estimation of the fair value of Alphabet Inc and the suggestion whether the firm may be a profitable choice for investment or not

- Finance assignment providing comparative ratio analysis of British Airways and Virgin Atlantic

- Finance assignment evaluating the reliance on EBITD Aand finding its alternatives

- (BUSM4741) Financial assignment analysing the financial statements of Kogan Com Ltd

- (BUSM1010) Finance assignment analysing the financial performance of Tassal Group Limited(TGR) and Motorcycle Holdings Limited(MTO)

- Finance Management assignment on tax havens for tax management

- (CBE6382) corporate financial management assignment exploring investment strategies for Mcdomalds

- financial resources management assignment for Aus Biotech

- (MBA6003)Finance assignment on adding value when capital markets are seen efficient

- Critical evaluation of the capital structure of Burberry in the finance assignment

- (SOE11444)The role of financial performance assignment research techniques towards determining financial performance measures and targets

- (BU7006)SWOT and PESTLE analysis strategic finance management assignment for JD group

- (BMG704) International finance assignment on the financial performance and the impact of two recent developments of Good year Tire & Rubber

- Financial Decision Making Assignment Focusing On The How Financial Decision Must Be Made By Organisation Heads

- (ACFI7013) International Finance Assignment: Questions and Answers

- Finance Assignment: Risk and Return Analysis in Corporate Finance

- (FIN200) Corporate Financial Management Assignment: Questions and Answers

- Finance Assignment: Impact of US Political and Economic Event on Australian Share Price

Looking for Your Assignment?

FREE PARAPHRASING TOOL

FREE PLAGIARISM CHECKER

FREE ESSAY TYPER TOOL

Other assignment services.

- SCM Assignment Help

- HRM Assignment Help

- Dissertation Assignment Help

- Marketing Analysis Assignment Help

- Corporate Finance Assignment Help

FREE WORD COUNT AND PAGE CALCULATOR

QUESTION BANK

ESCALATION EMAIL

To get answer.

Please Fill the following Details

Thank you !

We have sent you an email with the required document.

- Skip to main content

Schedule free consultation

SAMPLE COMPREHENSIVE FINANCIAL PLAN EXAMPLES

Personal financial plan examples.

Below are financial plan examples for hypothetical clients in several different situations. These plans were created by our Atlanta financial advisor team and should give you an idea of what is typically included in a plan. Hopefully, you’ll be able to find a sample plan that addresses issues you might be facing, and if that’s the case, the sample plan will provide you with a better understanding of the plan format, content and cost. Finding an Atlanta financial advisor who is a good fit can be difficult, so feel free to contact us for further information.

If, after reading the sample financial plans , you would like to attend a no-cost 90-minute workshop to create your own financial plan, click here . Please note that the workshop is only valid for U.S. residents, as all tax assumptions are based on U.S. tax regulations.

The personal financial plan examples below are just that – examples – and they aren’t meant to serve as advice. Your actual financial plan will depend upon your particular situation – your current resources, your goals and your return needs and risk tolerance among many other variables. The examples below include much of this information and cover the areas we typically address for in plans for clients with a particular need or at a specific stage in life. We typically present these plans over the course of two meetings that cover sixty to ninety minutes, during which we review a slide deck for each plan stage and answer any questions that may come up. Although not included in the sample plans below, we do create a to-do list at the end of the planning process so you’ll have a clear understanding of what needs to be done to implement your plan.

Example Financial Plan #1

Jack and Julie, a married couple whose kids are grown and financially independent, are planning on retiring in a few years

Jack and Julie are a few years away from retirement , and although there is some difference in their ages, they hope to retire simultaneously. Jack has worked for both the Federal Government and a state-run university, so he will receive two pensions in addition to the social security that they will both receive. Although Julie will not have a pension, she has saved aggressively in past years and will continue to save – albeit somewhat less aggressively – through retirement.

Jack and Julie believe that they are well situated for retirement, but they would like to better understand their financial position, and they have also prioritized survivor planning to confirm that they would both be fine should either pre-decease the other.

Financial Plan Outcome

As they suspected, Jack and Julie are in good shape for retirement, and after reviewing their plan results, they have begun to consider retiring earlier than they initially anticipated. They also have sufficient resources to financially weather a survivor situation, particularly if Jack receives an inheritance (as seems likely) from his father’s estate. Given Jack’s father’s long life, there is a higher than average chance that Jack will be long-lived, and if that is the case, it will be beneficial for him to delay taking social security.

Jack and Julie also completed a review of their other insurance coverages as well as their estate documents and existing portfolio allocation vs. the portfolio allocation used in the plan.

The retirement plan cost is $2640, and that included all work necessary to complete the plan as well as the two client meetings in which the plan was reviewed and discussed. Additionally, Jack and Julie had a few implementation questions after the final plan meeting that were covered in the fee as well.

Download Jack and Julie's Sample Financial Plan Today!

Get My Sample Financial Plan

Example Financial Plan #2

Sarah, a physician in her late 30’s focused on savings and planning for retirement.

Sarah is a doctor who works for a healthcare provider associated with a large university. She is single and in her late 30’s, and although her income has increased substantially since she completed medical school, her spending hasn’t followed suit. Thus, she is in the fortunate position of having substantial disposable income and the matching contributions from her employer to her retirement plans is generous.

She would like to retire in her mid-50’s, although she could put retirement off for a bit if necessary. In addition to contributing the maximum allowable amount to her retirement plans, she is also spending $15,000 each on paying down medical school debt and establishing an emergency fund. Sarah is seeking advice on whether or not her retirement goal is realistic, how best to achieve it and how she should invest.

Sarah is close to being on track, but she is more likely to be able to fully fund her retirement if she pushes it back to her late 50’s. Furthermore, her investments are a bit too conservative given her overall risk tolerance and return needs, so we recommend increasing her equity exposure. Lastly, she may want to consider additional disability insurance if it is available so that she can continue to meet her savings goals even in the event of long-term incapacity.

Financial Plan Cost

Sarah’s plan cost is $2,160. This cost included all work necessary to complete the plan, plus 2 client meetings to review the initial draft plan as well as the final plan, and subsequent support to answer any questions Sarah had as she worked to implement the plan.

Download Sarah's Sample Financial Plan Today!

Example financial plan #3.

David and Susan, a married couple in their late 30’s, both earn high incomes and recently made the decision to adopt twins

David and Susan are in a strong financial position, but the recent decision to adopt has led them to the decision to have a comprehensive plan done. Both David and Susan earn high incomes, and David works as a consultant while Susan splits time between research at a medical university and practicing at the university clinic .

David’s position requires a good deal of travel, and although he has no desire to retire early, he would like to find a less stressful job in his early 50s. Both David and Susan plan to continue working full time once the adoption is complete, and they may hire a nanny or consider daycare for the children. They have fundamental goals in planning: to adequately fund retirement and to fund education for the children. They want to ensure they are making optimal financial decisions and they would like to have the framework of a plan within which to make those decisions.

Plan Outcome

Given their high savings rate and low spending rate compared to their income, David and Susan are in a strong position. Nevertheless, their position can be strengthened by increasing their stock allocation slightly and by purchasing additional term life insurance to provide income to the surviving spouse in the event of premature death. We also recommend funding 529 plans to cover the educational goals, and we look closely at their various insurance coverages and methods they might use to minimize their tax liabilities.

Note that David recently became eligible for a deferred compensation plan that’s reserved for firm partners. However, the details of the plan are being finalized, and thus we have not included it here. Given its likely materiality, we would update the plan to include the deferred compensation once details are finalized.

David and Susan’s plan cost is $2640. Should they decide they want to work with Minerva on a retainer basis, the planning fee will be applied to the first quarter’s retainer fee.

Download David and Susan's Sample Financial Plan Today!

Understanding the financial planning process.

Many people look to a financial plan to be confident that they are on track for achieving their financial goals. They want to know that their financial goals and plan are realistic. Most importantly, however, they want to make sure that they’re making the best financial decisions and that they’ve prioritized their goals properly.

While many people are aware that they should have a financial plan, they might be unsure as to what the process looks like. At Minerva, we begin the financial planning process by finding out what’s most important to you and what you hope to accomplish. We’ll then focus on your short-term and long-term goals (like retirement and estate planning), and build a financial framework. When we establish your plan, we’ll give you a list of action items that you can follow to stay on track in your plan and if you work with us on an ongoing basis, we’ll work with you to ensure your plan is implemented and help you stay on track.

The sample financial plans we provide offer a glimpse into what is considered in some typical financial situations. Yet, it’s important to remember that your financial goals and situations are unique, and every financial plan is personalized. Our Atlanta financial advisor team has created plans for clients in a wide variety of situations, not just those shown above.

If you don’t find a plan above that is somewhat reflective of your situation, contact us to let us know a bit more about your situation.

Schedule a Complimentary 30-Minute Call to Discuss Your Situation

GET STARTED

Tax Season Savings

Get 40% off LivePlan

The #1 rated business plan software

Transform Tax Season into Growth Season

Discover the world’s #1 plan building software

Researched by Consultants from Top-Tier Management Companies

Powerpoint Templates

Icon Bundle

Kpi Dashboard

Professional

Business Plans

Swot Analysis

Gantt Chart

Business Proposal

Marketing Plan

Project Management

Business Case

Business Model

Cyber Security

Business PPT

Digital Marketing

Digital Transformation

Human Resources

Product Management

Artificial Intelligence

Company Profile

Acknowledgement PPT

PPT Presentation

Reports Brochures

One Page Pitch

Interview PPT

All Categories

Top 7 Financial Plan Templates with Examples and Samples

Prachi Soni

A financial plan is indispensable for both individuals and corporations. A well-crafted financial plan serves as a road map for achieving financial goals, managing income and expenses, and making sound investment, savings, and budgeting decisions.

Creating a financial plan from scratch, however, is a scary task. This is when financial plan templates come in handy.

As the starting point for a prosperous financial path, this article will examine the top seven financial plan templates, examples, and samples.

Each of the templates is 100% customizable and editable. The content-ready nature provides you with a starting point and a structure, the editability feature ensures the presentation can be tailored to unique audiences.

Seven Comprehensive Financial Plan Templates to Meet Objectives

Discover the key to financial success with our carefully curated selection of top seven financial plan templates, with real-life examples and samples. From budgeting and saving strategies to investment plans and retirement goals, each template offers a comprehensive framework tailored to specific financial objectives.

Template 1: Financial Planning PowerPoint Presentation Slides

A Financial Planning PowerPoint Presentation Slides Template helps presenters create an engaging and visually compelling presentation on budgeting, financial strategies, retirement planning, risk management, and more. By using this slide in your presentations on topics related to financial management, you will be able to save time and reduce required effort. Use this presentation template to showcase your expertise in 12 major segments of finance, including time value of money, inventory management, financial risk management and KPIs and dashboards that depict whether your financial plan worked or not . Master financial statements like those on income, cash flow and undertake a trend analysis as well. Even ratio analysis is covered. Take your financial planning presentations to the next level! Download this presentation template today!

Download Now!

Template 2: Financial Planning PowerPoint Template Bundles

Pitch yourself using this PPT slide to engage buyer personas and increase brand awareness. Due to the excellent graphics and content, these Financial Planning PowerPoint Template Bundles are perfect for interacting with your audience. This helps you present your financial planning and related topics effectively. Our ready-to-use slides are helpful for large and small companies. With these slides, you can easily explain your actual and budgeted expenses and income. Download it right away without any more delay.

Download Now

Template 3: Financial Planning Process Trusting Relationship Finance Information Analysis

This template provides a comprehensive framework for presenting fundamental concepts and steps involved in financial planning. It includes visually appealing slides covering goal setting, data collection, risk assessment, investment analysis, review & reports, and monitoring progress. Moreover, this template emphasizes trusting relationships with clients or stakeholders. Download now and become a standout presenter in the world of finance!

Template 4: Evaluating Company Overall Health with Financial Planning and Analysis PowerPoint

This PowerPoint template will boost your financial analysis presentations. This extensive deck covers many crucial financial planning and analysis topics. Introduce financial planning and your financial planning and analysis team. This template lets you demonstrate your expertise in assessing a company's financial health and providing insights for informed decision-making. Download now to enhance financial planning and analysis presentations.

Template 5: Financial Planning and Analysis Guide for Small and Large Businesses PowerPoint Presentation Slides

Chief financial officers (CFOs) will glean and provide pertinent business insights to their CEOs and other stakeholders for informed decision-making, where the role of money is significantly important. This is where our financial planning and analysis presentation comes into play. It will help businesses track financial health of their organizations and provide reliable guidance to business executives. The slides within the template are designed to be informative, visually appealing, and easy to understand . Download our expertly-crafted template and lead your company to more excellent financial health and success!

Download Here

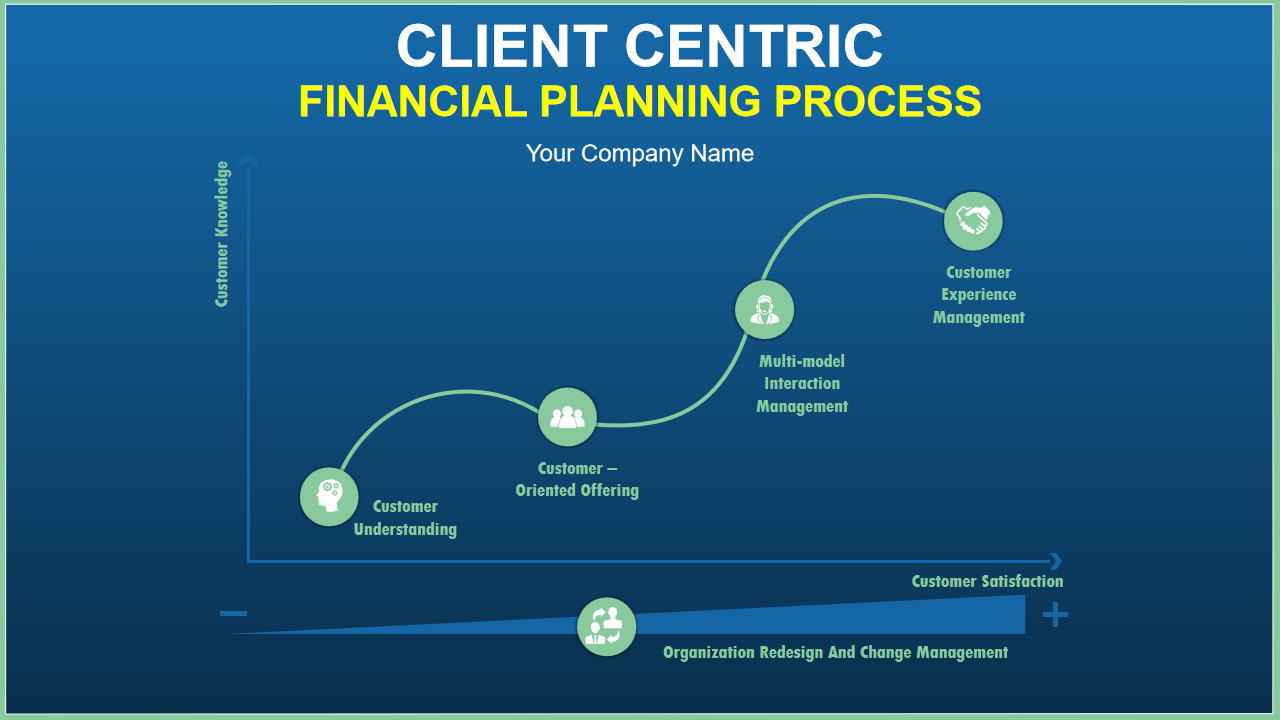

Template 6: Client-Centric Financial Planning Process PowerPoint Presentation Slides

Professionally designed to illustrate the client-centric financial planning process, the "Client-Centric Financial Planning Process PowerPoint Presentation Slides" are available for your next presentation. The purpose and benefits of financial planning are outlined in our PowerPoint presentations, which may be used to brief personnel. Professionals may wow clients with their ability to assess their needs, coordinate their efforts, and deliver customized, bespoke financial solutions using these slides in their presentations. Download our PowerPoint Presentation today to impress your audience!

Template 7: Financial Planning in Healthcare PPT Presentation Slides

Use this slide to implement best practices and establish monitoring criteria. Use our hospital budget planning PPT Templates to showcase latest financial trends in the healthcare sector, including value-based payments, data analytics, and upgraded financial leadership models. Compare current healthcare costs to future projections. Drive economic efficiency and stay ahead in the ever-evolving healthcare landscape. Download now and revolutionize your healthcare financial planning presentations.

TAKE CONTROL OF YOUR FINANCIAL FUTURE

This blog post reviewed top seven financial plan templates with examples. It improves financial planning for individuals and businesses. These templates can accommodate many needs and interests with features like thorough financial analysis and client-focused methods.

Remember that you need a sound financial plan to meet your financial goals, lower risk, and secure your future. It aids decision-making, adaptability, and financial success.

Choose the most effective option, make it your own so you can achieve your goals, and make the most of your financial planning procedure.

Take control of your financial future today! Discover the essential steps of personal financial planning and unlock the key to financial security. Download our comprehensive guide on How to Do Personal Financial Planning to Secure Your Future .

FAQs on Financial Plan Templates

What is a financial plan example.

A financial plan example is a sample or template demonstrating how a comprehensive financial plan is structured and organized. It includes components and sections that covers varied aspects of personal or business finances.

What are the seven categories of a financial plan?

A comprehensive financial plan covers many critical areas of a person’s or organization’s financial goals and plans. Seven financial plan types are:

- Cash Flow Management : A stable financial situation is maintained by making a budget, keeping track of income and spending, and managing cash flow.

- Includes insurance , money for emergencies, and planning to manage risks, if something goes wrong.

- Investment planning is the process of deciding how to make money through investments based on goals, risk tolerance, and time frame.

- Planning for retirement : Retirement planning is calculating how much money you’ll need to retire comfortably, planning out how you'll spend your time in retirement, and sticking to that plan.

- Tax Planning : Tax deductions, tax credits, and tax structures that are easy to understand can help lower your tax bill.

- Estate planning includes using wills, trusts, and powers of attorney to give away assets after death and keep taxes as low as possible.

- Financial Goals and Objectives : In this area, you can set financial goals like buying a home, paying for school, or starting a business and plan to reach them.

What are the five components of a financial plan?

A financial plan usually comprises a few essential parts that work together to make a complete plan for reaching financial goals. These are:

- Financial Goals : Clear financial goals give the plan direction and a reason for being. Some goals are short-term, like paying off debt, and some are long-term, like saving for retirement or a child's college.

- Budgeting and Cash Flow Management : Making a budget help keep track of income and spending, which lets people or groups use their resources in the best way possible. By looking at cash flow, you can see where you can save money, pay down debt, and build an emergency fund.

- Risk management : This part concerns keeping yourself safe from possible threats and uncertainties. It involves figuring out what kind of insurance you need (e.g., life, health, property), checking what you already have, and thinking about ways to reduce financial risks, like emergency funds and backup plans.

- Planning for investments means coming up with a plan to make money grow over time. This part looks at risk tolerance, time frame, and financial goals to determine the right asset allocation and investment tools (like stocks, bonds, and mutual funds).

- Planning for retirement : Planning for retirement ensures you have enough money when you stop working. It involves figuring out how much money you will need in retirement, how much you can save, how much you can contribute, and choosing retirement accounts like 401(k)s and IRAs.

Related posts:

- Top 10 Business Development Strategy Templates with Samples and Examples

- Top 5 Business Plan Timeline Template with Samples and Examples

- Top 10 Product Launch Timeline Template with Examples and Samples

- Top 7 Corporate Strategy Templates with Samples and Examples

Liked this blog? Please recommend us

Must-have Weekly Goals Templates with Samples and Examples

Top 5 Internal Audit Report Templates with Samples and Examples

This form is protected by reCAPTCHA - the Google Privacy Policy and Terms of Service apply.

Digital revolution powerpoint presentation slides

Sales funnel results presentation layouts

3d men joinning circular jigsaw puzzles ppt graphics icons

Business Strategic Planning Template For Organizations Powerpoint Presentation Slides

Future plan powerpoint template slide

Project Management Team Powerpoint Presentation Slides

Brand marketing powerpoint presentation slides

Launching a new service powerpoint presentation with slides go to market

Agenda powerpoint slide show

Four key metrics donut chart with percentage

Engineering and technology ppt inspiration example introduction continuous process improvement

Meet our team representing in circular format

5 Star Rating

Orders Deliver

PhD Experts

Top Quality

- / samples /

Financial Plan Assignment

Sample details.

Number Of View : 73

Download : 0

Words : 458

How useful do you think a financial plan is, considering that it is based on future assumptions that usually will not be 100% correct?

How valuable is it for the entrepreneur to evaluate and monitor financial plans monthly rather than waiting for quarterly reports?

In addition to your main response, you must also post substantive responses to at least two of your classmates' or instructor’s posts in this thread. Your response should include elements such as follow-up questions, further exploration of topics from the initial post, or requests for further clarification or explanation on some points made by your classmates.

Providing evidence or information from external sources in your posts will strengthen the points you are making and improve your overall score on the weekly Discussion Board activity.

The usefulness of a financial plan

A financial plan includes estimated profit and loss statement and cash flow statement of the business for the next 3 to 5 years. Sometimes, a balance sheet is also included in the financial plan. Thus, it helps the business to understand the financial capacity of the business and its potential to cover the cost of the business (da Silva Nogueira and Jorge, 2017). The financial plan is also important because, with the help of it, the business can establish a financial goal of the business and can develop strategies to achieve the goal. The financial plan also determines the feasibility of the business and tells the entrepreneur whether the business will be successful or not. The financial plan makes it clear that whether the resources are accessible or out of reach that can determine the success of the business. The financial plan is also useful for variance analysis because with the help of it the business can analyze its marketing plan and its potential to generate estimated revenue. The financial plan is also useful for forecasting and identifying financial requirements as well as obtaining funds for the business.

M onitoring financial plan monthly

The market is very volatile and changes are made frequently in the market and hence it is important to monitor the financial plan of the business so that the entrepreneur can make changes in the financial plan from time to time (Ghazali et al., 2018). If the entrepreneur will wait for the quarterly report, it cannot cope with the changes and hence may suffer loss. So, to avoid loss, it should be monitored and evaluated monthly rather than waiting for the quarterly report.

da Silva Nogueira, S. P., & Jorge, S. M. F. (2017). The perceived usefulness of financial information for decision making in Portuguese municipalities. Journal of Applied Accounting Research.

Ghazali, A. W., Suffian, M. T. M., Sanusi, Z. M., & Alsudairi, F. S. (2018). Managerial Opportunism: Monitoring Financial Risk of Malaysian Shariah-compliant Companies. GLOBAL JOURNAL AL-THAQAFAH, 99-115.

Place Order For A Top Grade Assignment Now

We have some amazing discount offers running for the students, get help instantly, free features.

Limitless Amendments

$09.50 free

Bibliography

$10.50 free

$05.00 free

$07.50 free

Plagiarism Report

$10.00 free

Get all these features for $50.00

Enter your email, and we shall get back to you in an hour.

This Website Uses Cookies Greatassignmenthelp.com respects the academic integrity guideline as per Australian norms. For reference purpose, our website contains sample and other related resources.

Business Financial Plan Example: Strategies and Best Practices

Any successful endeavor begins with a robust plan – and running a prosperous business is no exception. Careful strategic planning acts as the bedrock on which companies build their future. One of the most critical aspects of this strategic planning is the creation of a detailed business financial plan. This plan serves as a guide, helping businesses navigate their way through the complex world of finance, including revenue projection, cost estimation, and capital expenditure, to name just a few elements. However, understanding what a business financial plan entails and how to implement it effectively can often be challenging. With multiple components to consider and various economic factors at play, the financial planning process may appear daunting to both new and established business owners.