Receivables Finance And The Assignment Of Receivables

Do you want to know how access to trade finance can increase your cross-border imports and exports? Explore our Trade Finance hub for practical tools.

Are you a treasury or operations manager looking to mitigate the risks and efficiently manage your business’ cash flow? If so, check out our Treasury Management hub.

Whether you want updates from infrastructure support to cross-border transactions or clearing house operations to processing techniques, you can find all on our Payments hub.

Letters of Credit

Ready to to increase your imports / exports to guarantee the payment and delivery of goods? Find out more about LCs here.

Shipping & Logistics

Whether you’re transporting goods, or learning about supply chains, warehousing, transportation and packaging, we’ve got you covered.

Need to know which International Commerce Term is right for your needs? Explore our curated guides from shipping expert Bob Ronai.

Sustainability

Prioritising sustainable supply chains? Building inclusive trade? Working towards the UN’s 2030 SDGs? Read the latest on global sustainable standards vs green-washing here.

Heading into international markets? From the correct documentation to standardisation, here’s what you need to know for a streamlined customs clearance process.

TradeTech is rapidly evolving to help reduce some of the biggest challenges when it comes to trade. Keep up with these innovations here.

The latest in Trade, Treasury & Payments - stay up to date on all the changes across the globe.

The issues feature experts across the industry on the latest developments with specific themed and regional editions.

Insights by the industry, for the industry. These include thought leadership pieces, interview write ups and Q&As.

Working closely with industry experts and trade practitioners we provide inclusive educational guides to improve your technical knowledge and expertise in global trade.

Research & Data

We undertake qualitative and quantitative research across various verticals in trade, as well as create reports with industry association partners to provide in-depth analysis.

Trade Finance Talks

Subscribe to our market-leading updates on trade, treasury & payments. Join the TFG community of 160k+ monthly readers for unrivalled access in your inbox.

Welcome to Trade Finance Talks! On our series we hear from global experts in trade, treasury & payments.

Enjoy our bite-sized video content for insights on-the-go with our short VoxPop & summary series.

Experience the true nature of the TFG community through panel discussions on the latest developments - engage with questions.

Join us as we interview leaders in international trade, treasury, payments and more! Watch and learn.

Partner Conferences

We partner with industry conferences around the world to ensure that you don’t miss out on any event; in person or online, add to your calendar now.

Women in Trade, Treasury & Payments

Get involved in our most important campaign of the year, celebrating the achievements of women in our industry and promoting gender equity and equality.

Our excellence awards in trade, treasury, and payments are like no other. You can't sponsor them, and they're independently judged. They are the most sought-after industry accolades.

Online Events

Join our virtual webinars and community events. Catch up on-demand, right here on TFG.

Trade Finance

Trade finance is a tool that can be used to unlock capital from a company’s existing stock, receivables, or purchase orders. Explore our hub for more.

Invoice Finance

A common form of business finance where funds are advanced against unpaid invoices prior to customer payment

Supply Chain Finance

Also known as SCF, this is a cash flow solution which helps businesses free up working capital trapped in global supply chains.

Bills of Lading

BoL, BL or B/L, is a legal document that provides multiple functions to make shipping more secure.

A payment instrument where the issuing bank guarantees payment to the seller on behalf of the buyer, provided the seller meets the specified terms and conditions.

Stock Finance

The release of working capital from stock, through lenders purchasing stock from a seller on behalf of the buyer.

This allows a business to grow and unlock cash that is tied up in future income

Receivables Finance

A tool that businesses can use to free up working capital which is tied up in unpaid invoices.

Purchase Order Finance

This is commonly used for trading businesses that buy and sell; having suppliers and end buyers

Machinery & Equipment

Technology, construction, telecommunications, PPE, and electronics

Commodities & Materials

Raw materials, agricultural products, minerals, metals, and textiles

Chemical & Energy

Pharmaceuticals, chemicals, and energy products

Autos, Aerospace & Marine

Automotive, aviation, and marine industries

Pharma & Healthcare

Pharmaceuticals, healthcare equipment, and related sectors

Metals & Mining

Ores, minerals, metals, and concentrates

Finished Goods

Retail stock, e-commerce, textiles, clothing, and consumer goods

Construction & Projects

Construction, infrastructure, project finance, and green finance

Tech, Media & Telecom

Food & beverages.

Food, drink, dairy, confectionery, and alcohol

Professional Services

E-commerce, recruitment, legal services, and hospitality

Informing today's market

Financing tomorrow's trade

Soft Commodities Trader

Due to increased sales, a soft commodity trader required a receivables purchase facility for one of their large customers - purchased from Africa and sold to the US.

Metals Trader

Purchasing commodities from Africa, the US, and Europe and selling to Europe, a metals trader required a receivables finance facility for a book of their receivables/customers.

Energy Trading Group

An energy group, selling mainly into Europe, desired a receivables purchase facility to discount names, where they had increased sales and concentration.

Clothing company

Rather than waiting 90 days until payment was made, the company wanted to pay suppliers on the day that the title to goods transferred to them, meaning it could expand its range of suppliers and receive supplier discounts.

Get Trade Finance

Informing Today’s Market, Financing tomorrow’s Trade.

Trade Law Overview

Legal framework, finance facilities, emerging trends.

Access trade, receivables and supply chain finance

We assist companies to access trade and receivables finance through our relationships with 270+ banks, funds and alternative finance houses.

Download our free Digital Negotiable Instruments Initiative

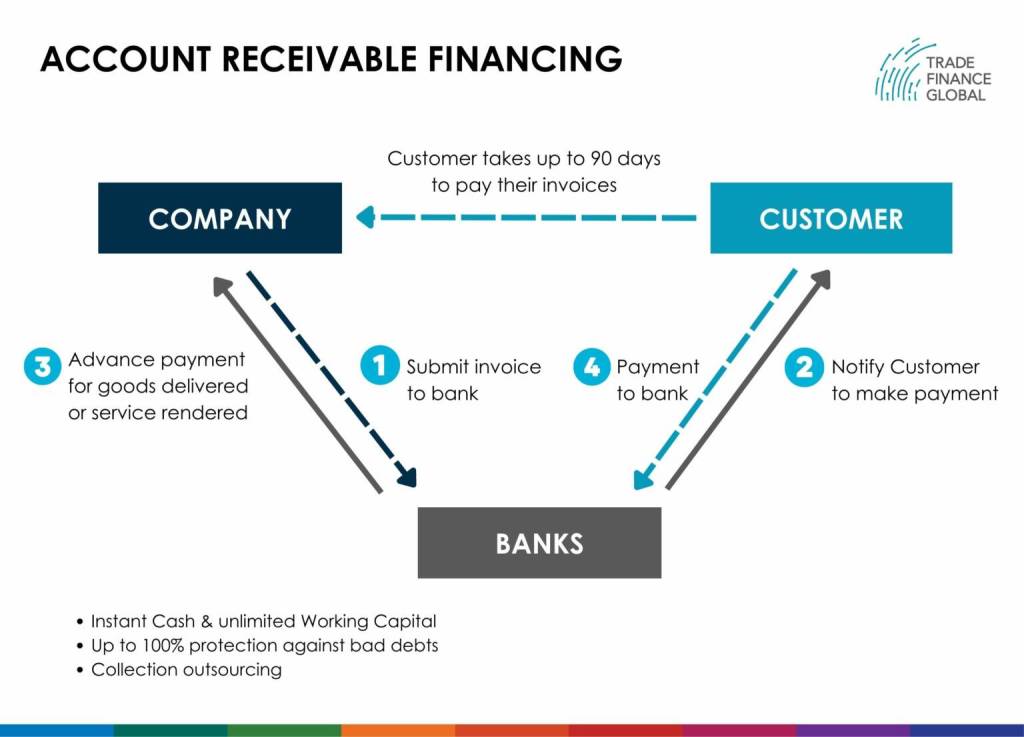

A receivable represents money that is owed to a company and is expected to be paid in the future. Receivables finance, also known as accounts receivable financing, is a form of asset-based financing where a company leverages its outstanding receivables as collateral to secure short-term loans and obtain financing.

In case of default, the lender has a right to collect associated receivables from the company’s debtors. In brief, it is the process by which a company raises cash against its own book’s debts.

The company actually receives an amount equal to a reduced value of the pledged receivables, the age of the receivables impacting the amount of financing received. The company can get up to 90% of the amount of its receivables advanced.

This form of financing assists companies in unlocking funds that would otherwise remain tied up in accounts receivable, providing them with access to capital that is not immediately realised from outstanding debts.

FIG. 1: Accounts receivable financing operates by leveraging a company’s receivables to obtain financing. Source: https://fhcadvisory.com/images/account-receivable-financing.jpg

Restrictions on the assignment of receivables – New legislation

Invoice discounting products under which a company assigns its receivables have been used by small and medium enterprises (SMEs) to raise capital. However, such products depend on the related receivables to be assignable at first.

Businesses have faced provisions that ban or restrict the assignment of receivables in commercial contracts by imposing a condition or other restrictions, which prevents them from being able to use their receivables to raise funds.

In 2015, the UK Government enacted the Small Business, Enterprise and Employment Act (SBEEA) by which raising finance on receivables is facilitated. Pursuant to this Act, regulations can be made to invalidate restrictions on the assignment of receivables in certain types of contract.

In other words, in certain circumstances, clauses which prevent assignment of a receivable in a contract between businesses is unenforceable. Especially, in its section 1(1), the Act provides that the authorised authority can, by regulations “make provision for the purpose of securing that any non-assignment of receivables term of a relevant contract:

- has no effect;

- has no effect in relation to persons of a prescribed description;

- has effect in relation to persons of a prescribed description only for such purposes as may be prescribed.”

The underlying aim is to enable SMEs to use their receivables as financing to raise capital, through the possibility of assigning such receivables to another entity.

The aforementioned regulations, which allow invalidations of such restrictions on the assignment of receivables, are contained in the Business Contract Terms (Assignment of Receivables) Regulations 2018, which will apply to any term in a contract entered into force on or after 31 December 2018.

By virtue of its section 2(1) “Subject to regulations 3 and 4, a term in a contract has no effect to the extent that it prohibits or imposes a condition, or other restriction, on the assignment of a receivable arising under that contract or any other contract between the same parties.”

Such regulations apply to contracts for the supply of goods, services or intangible assets under which the supplier is entitled to be paid money. However, there are several exclusions to this rule.

In section 3, an exception exists where the supplier is a large enterprise or a special purpose vehicle (SPV). In section 4, there are listed exclusions for various contracts such as “for, or entered into in connection with, prescribed financial services”, contracts “where one or more of the parties to the contract is acting for purposes which are outside a trade, business or profession” or contracts “where none of the parties to the contract has entered into it in the course of carrying on a business in the United Kingdom”. Also, specific exclusions relate to contracts in energy, land, share purchase and business purchase.

Effects of the 2018 Regulations

As mentioned above, any contract terms that prevent, set conditions for, or place restrictions on transferring a receivable are considered invalid and cannot be legally enforced.

In light of this, the assignment of the right to be paid under a contract for the supply of goods (receivables) cannot be restricted or prohibited. However, parties are not prevented from restricting other contracts rights.

Non-assignment clauses can have varying forms. Such clauses are covered by the regulations when terms prevent the assignee from determining the validity or value of the receivable or their ability to enforce it.

Overall, these legislations have had an important impact for businesses involved in the financing of receivables, by facilitating such processes for SMEs.

Digital platforms and fintech solutions: The assignment of receivables has been significantly impacted by the digitisation of financial services. Fintech platforms and online marketplaces have been developed to make the financing and assignment of receivables easier.

These platforms employ tech to assess debtor creditworthiness and provide efficient investor and seller matching, including data analytics and artificial intelligence. They provide businesses more autonomy, transparency, and access to a wider range of possible investors.

Securitisation is an essential part of receivables financing. Asset-backed securities (ABS), a type of financial instrument made up of receivables, are then sold to investors.

Businesses are able to turn their receivables into fast cash by transferring the credit risk and cash flow rights to investors. Investors gain from diversification and potentially greater yields through securitisation, while businesses profit from increased liquidity and risk-reduction capabilities.

References:

https://www.tradefinanceglobal.com/finance-products/accounts-receivables-finance/ – 28/10/2018

https://www.legislation.gov.uk/ukpga/2015/26/section/1/enacted – 28/10/2018

https://www.legislation.gov.uk/ukdsi/2018/9780111171080 – 28/10/2018

https://www.bis.org/publ/bppdf/bispap117.pdf – Accessed 14/06/2023

https://www.investopedia.com/terms/a/asset-backedsecurity.asp – Accessed 14/06/2023

https://www.imf.org/external/pubs/ft/fandd/2008/09/pdf/basics.pdf – Accessed 14/06/2023

Speak to our trade finance team

- International Trade Law Resources

- All International Trade Law Topics

- Conferences

Assignment of Receivables – The Achilles’ Heel of Invoice Financing

Receivables are a key tool in trade finance particularly with the use of invoice financing. By transferring the rights to a receivable such as an invoice, SMEs are able to get much needed working capital, getting paid by funders today, what is owed by their buyers in the future. Whether done on a recourse or non-recourse basis, assignments of the receivables are a central feature of invoice finance structures as they give funders critical rights against buyer-debtors. But without sufficient care on how assignments are obtained, this simple document can be the Achilles’ heel of an invoice financing program.

Risks in Invoice Financing

Invoice financing transforms a supplier-buyer relationship into a multi-faceted, funder-buyer as well as funder-supplier dynamic. The risks to be considered include:

- Receivable title risk: the risk that the supplier may have already assigned or pledged the receivable to another funder;

- Receivable transfer risk: the risk that applicable law may not allow the funder to take good title to the receivable, or otherwise subordinate the lender’s rights to third party claims;

- Dispute risk: the risk that the buyer may claim the supplier failed to deliver goods in accordance with the contract;

- Discount or dilution risk: the risk that the buyer will not pay the full amount of the invoice for reasons other than the supplier’s performance of the contract e.g., relying on set-off rights or discounting mechanisms in umbrella arrangements unknown to the funder;

- Payment delay risk: the risk that the buyer will not pay on time;

- Payment direction risk: the risk that the buyer will make the payment to the supplier or some other party instead of the funder; and

- Debtor credit risk: the risk that the buyer-debtor does not pay at all.

Assignments – why are they important.

A robust invoice financing program using assignments should narrow the risks above but only if careful attention is paid to how they are done. When assigning an invoice, a notice of the assignment serves both legal and practical functions. Legally, a notice of assignment is one of the requirements to create a legal assignment, which in turn allows the assignee-funder to enforce rights in its own name. Without notice, the assignment is treated as an equitable assignment which may provide challenges for a funder to enforce rights through an uncooperative supplier. Practically, a notice also serves to “flush out” some common excuses a buyer may deploy for non-payment relating to setting-off sums from other transactions, side arrangements on discounting or disputes relating to the invoice itself.

With no visibility on whether receivables had been previously assigned, a notice of an assignment serves as an important basic risk mitigant towards double financing. In addition, in cases of multiple assignments done by the supplier, a notice serves to give priority to a funder against subsequent funders – this can make all the difference if multiple financing of the same invoice is discovered later.

Forged/ Multiple Assignments

A notice of assignment as acknowledged by the buyer is only half the battle. In a pursuit for liquidity, unscrupulous traders may fabricate contracts, invoices and by extension assignment acknowledgements. These illegitimate acts may sometimes never come to light as a supplier may be able to recycle liquidity in time to repay its funders. But other times, forged acknowledgments or multiple financing are only discovered when the funder seeks to enforce against the buyer, who may be located in a difficult jurisdiction to get effective legal recourse. In the process, startling discoveries can be made:

- The buyer alleges the contract, invoice and acknowledgment of assignments have been forged;

- The buyer alleges that goods were never received notwithstanding invoicing and acknowledgment of the assignment of the invoice;

- The buyer is directed by the supplier to pay the supplier directly or a third party notwithstanding the assignment notice;

- The buyer convinces the supplier that the assignment has been extinguished; or

- The same invoice has been assigned to multiple funders.

The Achilles’ heel with assignments in invoice financing programs is that there is little interface between the funder and the buyer – the supplier plays a central role in routing documents to its funder. Funders have little visibility or capacity to verify every document and even where verification is done, an unscrupulous supplier may still impersonate their buyers with fictitious email accounts. The difficulty in detecting invoice fraud cannot be overstated and will continue to challenge the trade finance market. The Association of Banks in Singapore have introduced a Code of Best Practices for commodities financing which includes recommendations to get some reference of an assigned invoice into the invoice document itself and for lenders to obtain acknowledgment of assignments directly from the buyer. But without a registry for invoices, it would be difficult for funders to eradicate multiple assignments of the same receivable. Singapore is making plans to change that – so do watch this space.

Assignments as security or as outright transfer – why does it matter?

A receivable can be assigned as security for performance of a supplier’s obligation to repay a loan. Alternatively, an assigned receivable can operate as an outright transfer to a funder. The distinction is critical as understanding which party has ownership in the receivable can have important accounting (e.g., off balance sheet treatment) and legal consequences (e.g., the right to sue under the invoice). The distinction is even more acute if the supplier goes into liquidation – if deemed a security, a receivable would be treated as part of the insolvent supplier’s assets and if the supplier fails to register its assignment as a charge, then it may be void against the liquidator with the consequence that the funder is left unsecured for its debt. Receivables Purchase Agreements, in trying to have the best of both worlds to protect the funder for every loss and contingency can often inadvertently run the risk of being reclassified as a loan rather than a “true sale”.

- August 2024

BG 5th Anniversary Party Photos

The law should call a fraud a fraud:, oil storage: considerations for financiers & traders.

70 Shenton Way, EON Shenton, #10-12, S079118

- +65 6970 1677

- [email protected]

- Subscribe to our mailing list

- More Blog Popular

- Who's Who Legal

- Instruct Counsel

- My newsfeed

- Save & file

- View original

- Follow Please login to follow content.

add to folder:

- My saved (default)

Register now for your free, tailored, daily legal newsfeed service.

Find out more about Lexology or get in touch by visiting our About page.

Legal considerations of assignment of receivables under Swiss international private law

When structuring securitisation transactions in an international context, putting a receivables transfer agreement in place reveals the existence of various legal concepts relating to the transfer of title to receivables in the relevant jurisdictions. Further, it becomes evident that the country-specific conflict of laws deviate considerably from each other with regard to the connecting factor which decides on the law governing the assignment. While some jurisdictions focus on the assignor's jurisdiction of incorporation, others focus on the law governing the respective receivables, as is the case for Switzerland. Prior to providing a quick overview of the legal position in Switzerland under a conflict of laws perspective, this article outlines some basic elements of substantive Swiss assignment law.

Transfer of title in receivables

Pursuant to Swiss substantive law, the assignment of receivables must be made in writing. In such respect, scanned copies of duly executed original copies of declarations of assignment do not qualify as instruments in writing. Thus, in principle, the assignment of a receivable is perfected only on the assignee's receipt of the original wet-ink copy of the duly executed declaration of assignment. With a view to electronic data transmission, under Swiss law the only equivalent to a handwritten signature is an authenticated electronic signature combined with an authenticated time stamp within the meaning of the Federal Act of 18 March 2016 on Electronic Signatures. However, in practice, electronic signatures have not yet become popular, as their application is rather sophisticated.

Further, all receivables to be subject of an assignment must be sufficiently specified. In order to ascertain compliance with this requirement, the declaration of assignment must comprise a list of the respective receivables, detailing at least the name and address of the respective debtor and the nominal amount, invoice date and due date for each receivable. In case of a repeat transfer of receivables, it must be ensured that the assignor is contractually obliged to periodically provide updated lists of the receivables, specifying each receivable individually.

Notification of assignment to debtors: no perfection requirement

There is no perfection requirement for the notification of debtors of receivables under mandatory Swiss law. However, prior to the notification of an assignment, debtors may validly discharge their payment obligation by effecting payment to the originator of the receivables or a third party asserting title over the receivables, subject to the relevant debtor acting in good faith. However, the right to notify debtors qualifies as a right connected to ownership in the receivables. As a result, a contractual waiver by assignees of such rights for a certain period bears the risk that the assignment will qualify as a conditional assignment only to the detriment of the assignee in particular in an insolvency scenario.

Law on assignment of receivables: Swiss conflict of laws rules

As a general rule under Swiss conflict of laws rules, the transfer and assignment of a receivable will be governed by the law governing such receivables. However, the Swiss Private International Law Act of 18 December 1987 (PILA) allows for a choice of law (ie, a law other than that governing the receivables to be transferred and assigned) to govern the assignment between assignors and assignees. In such respect, according to Article 145 of the PILA, a choice of law clause regarding the assignment of a receivable may not be asserted against the debtor of the assigned receivable, not having agreed to such choice of law. According to the PILA, except where a debtor consents, a Swiss law-governed assignment of a receivable that is governed by a law other than Swiss law will not replace, affect or alter the foreign law applicable with respect to the debtor's rights and obligations pursuant to the receivable which continues to be determined in accordance with the relevant foreign law provision. As a consequence, the assignment of a non-Swiss receivable under Swiss law is valid and enforceable only between the parties to the assignment agreement.

Formal requirements regarding the assignment are subject only to the law governing the assignment agreement.

From a Swiss legal perspective, in order to ascertain the enforceability of an assignment against a debtor of receivables, the assignment of a receivable must be subject to the law governing the respective receivable. Further, in order to safeguard the validity of a Swiss law-governed assignment of receivables under a formalities perspective, care must be taken that a wet-ink original of each declaration of assignment is made available to the assignee. When using electronic signatures, a careful check of the validity of such signatures is key, as in practice, such signatures often lack one of the required elements which becomes apparent only on running a careful search using the relevant tools.

Filed under

- Switzerland

- Securitization & Structured Finance

- Walder Wyss Ltd

Popular articles from this firm

A general introduction to employment law in switzerland *, article 725 et seq. co: (il-)liquidity, capital loss and over-indebtedness - new duties for swiss boards *, besserer schutz des anwaltsgeheimnisses bei internen untersuchungen *, a general introduction to tax disputes and litigation in switzerland *, better protection of attorney-client privilege in internal investigations *.

If you would like to learn how Lexology can drive your content marketing strategy forward, please email [email protected] .

Related practical resources PRO

- How-to guide How-to guide: How to comply with climate-related regulations applicable to the financial services sector in the UK

- Checklist Checklist: GDPR compliance self-assessment audit (EU)

- How-to guide How-to guide: How to prepare for and respond to a governmental investigation or enforcement action for violation of US privacy laws (USA)

Related research hubs

- Insights & events

The Business Contract Terms (Assignment of Receivables) Regulations 2018 - back for good?

In an illustration that if at first you don’t succeed, you should try and try again, the UK government has published a revised draft of the regulations designed to prohibit contractual clauses which prevent one party from assigning its right to payment to a third party.

The first iteration of these regulations, designed to open up invoice finance to smaller businesses by removing contractual restrictions, was published back in December 2014. However they were viewed as having various flaws and the government went back to the drawing board. Last September saw the publication of The Business Contract Terms (Assignment of Receivables) Regulations 2017 only for the same to be withdrawn before year-end because of a perception that they still required further work.

Below we provide a summary of the key features of The Business Contract Terms (Assignment of Receivables) Regulations 2018. However before we continue it’s worth highlighting two specific exemptions from the draft legislation.

Two key exemptions

Firstly, the regulations do not apply to contracts to acquire a business or an interest in a firm. This removes the previous uncertainty as to whether or not the general prohibition outlined below would apply to restrictions on assignment contained in share and business sale agreements. Under the draft of the regulations, it will not.

Secondly, contracts entered into by a project company of a project which is a public-private partnership project, a utility project or a financed project are also exempt from the draft regulations. This may be in response to previous feedback on the earlier draft of the regulations. In particular, in its response to The Business Contract Terms (Assignment of Receivables) Regulations 2017, The City of London Law Society (CLLS) noted that prohibitions and restrictions on assignment (including assignment of receivables) are common in construction contracts, such as the JCT suite of contracts, because developers wish to ensure that the money they spend goes to the subcontractors and suppliers undertaking the work on a given project.

The CLLS expressed the view that the previous draft of the regulations had the potential to create uncertainty and market disruption in a wide range of transactions in the building infrastructure and energy construction markets in the UK. Whether the revised draft of the regulations adequately address such concerns remains to be seen (as at the date of this alert, the CLLS has not yet published any response to the latest regulations).

Overview of The Business Contract Terms (Assignment of Receivables) Regulations 2018

If approved by Parliament, the regulations would provide as follows:

- General prohibition : regulation 2 of the draft regulations sets out a general prohibition which says that “ a term in a contract has no effect to the extent that it prohibits or imposes a condition, or other restriction, on the assignment of a receivable arising under that contract or any other contract between the same parties ”. In broad terms, this means that a term contained in a contract between parties A and B, under which party A pays sums to party B in return for the supply of goods or services by party B to party A, but which prevents party B from assigning that payment right to non-party C, will have no effect.

- Anti-avoidance : the draft regulations also include provisions which are designed to prevent contract parties from circumventing the general prohibition outlined above by preventing an assignee of a payment right from determining the validity or value of the receivable or their ability to enforce the receivable. To this end, the draft regulations list 13 different categories of information which, if the assignee is unable to obtain such information by reason of a restriction in a contract, then such contractual restriction will also be of no effect. These categories of information include (among other things) the names of the contract parties, the relevant goods, services or other assets which give rise to the receivable, the amount payable (including any VAT chargeable), any applicable discount and the credit period applicable to the receivable. So, using the previous example, if a contract entitled party B to assign its receivable to non-party C but did not allow party B to disclose any of the foregoing details regarding such receivable to non-party C, then under the draft regulations such contractual restriction would also be of no effect.

- Exception for suppliers which are large enterprises or SPVs : regulation 3 of the draft regulations provides that the general prohibition outlined above does not apply, and accordingly contractual restrictions which prevent the assignment of a receivable shall continue to have effect, if at the time of the assignment the supplier (i.e. the creditor) is a large enterprise or a special purpose vehicle. In practice, this will allow smaller businesses to continue to impose restrictions on assignment when contracting with large businesses. The regulations go on to clarify what is meant by a “large enterprise” which, in broad terms, includes any company or limited liability partnership unless it is a small or medium-sized business and is not a member of a large group. So, the regulations would apply if, using our previous example, party B (the supplier) is a company to which the small companies regime (within the meaning of sections 381-384 of the Companies Act 2006) applied in the last financial year (before the date on which the receivable is assigned) in respect of which the supplier filed accounts. The opposite would be true if party B failed to satisfy any one or more of the conditions which mark out a small or medium-sized business from a large one in regulation 3 of the draft regulations.

- Exempt contracts : as with previous iterations of the proposed regulations, the draft regulations continue to exempt certain kinds of contracts from their scope. As well as those highlighted under the first heading above, the regulations do not apply to contracts for prescribed financial services, contracts concerning any interest in land, consumer contracts, petroleum licences, contracts concerning a matter of national security, securities options, forwards, swaps and other derivatives.

- Territorial application : the draft regulations would only apply to contracts governed by English law. There are deeming provisions which provide that the regulations would still apply where parties deliberately adopt the governing law of a country outside of the United Kingdom in order to evade the operation of the regulations.

If the draft Business Contract Terms (Assignment of Receivables) Regulations 2018 do receive Parliamentary approval, they would apply to contracts entered into on or after 31 December 2018. Watch this space to see if they do finally make it past the finishing post in their latest guise.

Contact our experts for further advice

Necessary cookies . These are cookies which are necessary for the operation of our website. We set these cookies so that they are always on.

Analytics and other third-party cookies . We would like to use analytics and limited other third-party cookies to improve our website and your experience using it. These cookies collect and report information to us about your browsing activity on our website. If you are happy to allow us to use these cookies, please click “all cookies” or you can turn individual cookies on by clicking "manage cookies". You can change your preferences at any time by visiting our cookie details page.

We use cookies on our website, details of which are set out below.

Necessary cookies

These are cookies which are necessary for the operation of our website. We set these cookies so that they are always on, although you may be able to disable these cookies via your browser if you wish. Please note that if these cookies are disabled then you may not be able to use some or all of the functionality of our website.

Ideally over time we would like to be able to improve our website and your experience using it. We would like to deploy analytics cookies to enable us to do this, which would collect and report information to us about your browsing activity on our website. However, we will only use these cookies with your consent and these cookies are switched off until you opt to turn them on. Click here for a full list of analytics cookies used on our website.

Third-party cookies are set by our partners and help us to improve your experience of the website. Click here for a full list of third-party plugins used on our website.

Search our site

Trending News

Related Practices & Jurisdictions

- Bankruptcy Restructuring

- Litigation Trial Practice

- Administrative Regulatory

- European Union

The validity of an assignment of receivables cross-border depends on the law that applies to the assignment.

What might amount to a valid assignment in one jurisdiction does not mean that it is valid in another, and where there are competing claims to the receivables and competing jurisdictions, the question of which law applies - and therefore whether there has been a valid assignment - significantly affects the ability of the assignee to rely on the assignment.

This question arose in the context of a German bankruptcy where the issue was referred to the European Court of Justice (“ECJ “) for a preliminary ruling. The recent decision of the ECJ of 9 October 2019 surprised many because it went against the commonly held view that in determining jurisdictional questions Article 14 of the European Union Rome I Regulation applied.

In this blog we consider the implications of the ECJ judgment in Case C-548/18 BGL BNP Paribas SA vs. TeamBank AG Nürnberg and how this affects assignees and the priority of competing claims. We also consider the proposed EU Assignment Regulation and how that might assist in determining the question of jurisdiction in the future.

A national of Luxembourg (the “employee”) but resident of Germany was employed by a Luxembourg employer under Luxembourg law. A German bank granted a German law governed loan to the employee and the employee assigned to the German bank all its claims to receive remuneration from the Luxembourg employer.

Three months later the employee obtained another loan, this time from a Luxembourg bank and assigned the same remuneration claims as security for that second loan to the Luxembourg bank under a Luxembourg law governed assignment contract. The Luxembourg bank notified the assignment to the Luxembourg employer, the German bank did not do so.

The employee became insolvent and German insolvency proceedings were commenced.

Under German law notification of an assignment is not required to perfect the assignment, but under Luxembourg law it is. Accordingly, in this case if German law applied the assignment to the German bank would have had priority over the assignment to the Luxembourg bank but if Luxembourg law the priority position would have been reversed.

Which law therefore took precedence? The German court requested the ECJ give a preliminary ruling on the question. Contrary to the commonly held view, the ECJ concluded that Article 14 of the Rome I Regulation did not assist and was therefore unable to provide for an answer to the question leaving the German court in a challenging situation particularly so, because the relevant rules for determining the conflict of law were actually deleted from German law in 2009.

So which law do the courts apply when determining whether there has been a valid cross-border assignment of receivables? Currently the answer depends on which country is being asked to consider the question:

(i) It could be the law which is expressed to govern the contract from which the assigned receivable arises. This is the approach normally adopted in Germany.

(ii) In England, the Netherlands and Spain it is in principle the law chosen by the assignor and the assignee to govern the contract under which the receivable is assigned;

(iii) Whereas in the U.S., for example it is in principle the law of the jurisdiction in which the assignor is situated.

The position is far from clear meaning that an assignees of receivables cannot always be certain whether the assignment is valid and enforceable.

Hope for the future? -The proposed EU Assignment Regulation

Thankfully the European Union intends to introduce new legislation that will help clarify the position. The Assignment Regulation proposed in March 2018 is currently being discussed in the Council of the European Union. However it is likely to be subject to extensive negotiation before adoption.

The principles set out in Article 4 of the Assignment Regulation are that the law of the habitual residence of the assignor will apply (Article 4 (1)) unless:

the claim is cash credited to a bank account or claims arising from financial instruments, in which case the law governing the account or the financial instrument will apply (Article 4 (2)), or

there is a securitization, in which case the assignee and the assignor can chose the law applicable to the assignment (Article 4 (3)).

Once adopted (subject to a 18 month waiting period) the Assignment Regulation will be directly applicable. This means that whilst EU Member States do not need to implement it into their domestic laws the courts of the Member States are bound to apply it in respect of all assignments which are concluded on or after the date it comes into effect.

However, the Assignment Regulation will not apply in Denmark, it will only apply in Ireland if Ireland opts into the Assignment Regulation and will not apply to the UK since it is expected that the UK will no longer be a EU Member State at the time the regulation is adopted and becomes effective.

The Assignment Regulation does not allow parties to contract out of it or to agree the applicable law which shall regulate the assignment of claims.

Major impact on international trade finance

The Assignment Regulation is expressed to have Universal Application, which means that it will apply the law designated by the assignment, even if this is not the law of any Member State.

For example, if a US exporting company assigns an invoice or other claim arising from a contract governed by German law to an EU assignee, then US law will apply in determining whether the assignment was effective vis-à-vis third parties, and not German law.

Because of this rule the Assignment Regulation will have a major impact on international trade finance involving the assignment of receivables. It could also create uncertainty over which law is applicable if the relevant third country’s law does not recognize the rule contained in Article 4(1).

What is the effect of the Assignment Regulation on Bank Accounts?

Bank accounts and account pledges will continue to be governed by the law of the country where the relevant bank is situated, provided that the account mandate prescribes that the law of that country shall govern the banking relationship.

However, this will only apply to bank accounts held with banks where the head office is situated within the European Union and to branches of third country banks which are located within the European Union.

In respect of banks situated outside of the European Union Article 4 (1) applies and the relevant account security will be governed by the law of the country where the bank has its place of central administration. .

What is the effect of the Assignment Regulation on Financial Instruments?

The law that applies to Financial Instruments will be the law governing the instrument. Article 2 (i) of the Assignment Regulation defines “Financial Instrument” as the instruments specified as such in the MIFID II Directive (Section C of Annex I of Directive 2014/65/EU of 15 May 2014).

It is unclear how this will affect the German Schuldschein -Market, since Schuldscheine with a term of more than 397 days may not qualify as a Financial Instrument. This could mean that secondary trading in such Schuldscheine becomes quite complex since the assignment of the relevant Schuldscheine will not be governed by German law, but by the law of the jurisdiction where the previous holders of the Schuldscheine is situated – and this could be any number of jurisdictions

What is the effect of the Assignment Regulation on securitization?

Presently the Assignment Regulation provides that the assignor and the assignee of a receivable/claim may choose the law applicable to the assignment of the securitization. However, the European Parliament propose to delete this exemption. This is disappointing because the proposal made by the European Commission could make securitization much easier and less complex than is currently the case.

What is the position in respect of Factoring, Asset Based Lending and Invoice Discounting?

Article 4(1) will apply to all other forms of receivable finance such as factoring, asset based lending, invoice discounting or other forms of supply chain finance. Accordingly the law of the central place of administration of the assignor determines the effectiveness and perfection of the assignment vis-à-vis third parties.

In practice that rule will make the financing of portfolios of receivables (which could be subject to a multitude of jurisdictions) much easier, where they are owned by one assignor situated in one jurisdiction. In that case it will be much easier to identify the one relevant law applicable.

Conversely, it will make it more difficult to finance portfolios of those receivables where assignors are situated in various jurisdictions but the receivables themselves are governed by the same law.

How does the Assignment Regulation apply to cross-border assignments in insolvency?

The difficulty here, is that the relevant test for the purposes of Article 4(1) of the Assignment Regulation in determining the “habitual residence” of the assignor is the “ place of central administration ” whereas the test under the EU Insolvency Regulation is the “centre of main interests” (COMI) and the presumption that the COMI is the company’s registered office. There is no such assumption under the Assignment Regulation.

Applying either of those tests may result in the same answer but it cannot be excluded that the location of the assignor could be different in some circumstances, resulting in uncertainty as to which law might apply to cross-border assignments in insolvencies.

Further, unlike under the EU Insolvency Regulation where the definition of COMI requires the company to have held its centre of main interests for 3 months, the same does not apply under the Assignment Regulation. Therefore, it could make it difficult to identify the “place of central administration” if the assignor has recently changed location, and again, the ability to identify the relevant applicable law.

The principles set out in the Assignment Regulation are welcome because they provide much needed clarity on which law applies when determining the validity of an assignment of receivables cross-border. It will provide more certainty to assignees, and hopefully lead to less litigation as a consequence.

Current Public Notices

Current legal analysis, more from squire patton boggs (us) llp, upcoming legal education events.

Sign Up for e-NewsBulletins

This website will offer limited functionality in this browser. We only support the recent versions of major browsers like Chrome, Firefox, Safari, and Edge.

- Home News and Insights Assignment of Receivables

Assignment of Receivables

3rd November 2017

The draft Business Contract Terms (Assignment of Receivables) Regulations 2017 (the “ Draft Regulations “) are currently before Parliament. If approved, these would contain provisions to nullify contract terms which attempt to restrict the ability of a party to assign a receivable.

In December 2014, the Department for Business, Innovation & Skills (BIS) consulted on an earlier version of the Draft Regulations. These earlier regulations contained a provision that allowed a party to rely on a confidentiality clause to prevent assignment of a receivable. This was included in the event that a debtor is unwilling for a receivable to be assigned because the disclosure of the debt to a third party compromises the debtor’s confidentiality. In August 2015, BIS published a response to the consultation.

Businesses often have to wait for a considerable length of time to be paid, which can cause cash flow issues. As a way of raising finance, a business may choose to assign an unpaid invoice to a third party, such as an invoice finance provider. This works by the finance provider lending the money to the business on the basis that the invoice is assigned to the finance provider. The finance provider will then pursue the debtor for the unpaid amount which will cover the earlier loans to the business.

Most contracts contain boilerplate provisions preventing the assignment of any rights under the contract unless the other party consents. A receivable is a right to be paid and a boilerplate non-assignment clause is broad enough to prevent invoices from being assigned.

Certain contracts are excluded from these rules. These include contracts for: an interest in land; for financial services; consumers where one or more of the parties is acting for purposes which are outside a trade, business or profession; for national security; and for certain energy and petroleum contracts.

Noticeably, the Draft Regulations do not include the confidentiality clause that was included in the earlier version.

Controversially, “assignment” is not defined. It is clear that this law would apply to outright assignments of receivables, but it is unclear the extent which it will apply to security interests. On the face of it, the new law will extend to security assignments but not charges or trusts. This may have the result that the parties cannot prevent a security assignment but can prevent a lesser interest such as a charge.

One of the reasons why restrictions on assignment are included in contracts is to protect the payer from having to pay more to an assignee than it would have to pay to the assignor. However, there is nothing in the Draft Regulations to protect the payer. It can only rely on its rights under the general law, which are extensive but not as good as an effective prohibition on assignment.

If approved, the Draft Regulations will not only apply to small companies. It will also read so that it covers all contracts, including those in existence at the time the new law comes into effect, which is expected to be in November or December 2017.

Related Blogs

Court provides further clarity on managing employees who express potentially offensive beliefs

The Bick Inquiry: comprehensive second phase to be published this September

Labour law impacting the UAE K-12 sector

Recent migration changes impacting employers

Chohan v Ved: the High Court Ruling and what it means for directors

India’s new criminal legalisation: prioritising justice over punishment

Bombay High Court Quashes FIR and chargesheet against directors towards delay in depositing Provident Funds

Service charges and gratuities: tips on tips

Introducing Spain’s startup law

Social media – friend or foe in the healthcare profession?

Is the CQC being a “dash” reliant on service user voice?

The Legal and Safety Challenges in the Anticipated UK Housing Boom

Sign up for useful insights straight to your inbox.

- News & insights

- Non-assignment claus…

- Share this page

Andrei Babiy

- On this page

8 December 2020

Non-assignment clauses in Dutch law: the end of the road?

On 2 June 2020, an act to abolish the practice of contractually agreeing prohibitions/restrictions on the transfer or pledging of receivables – insofar as they have been obtained in the exercise of a profession or business – was submitted to the House of Representatives (the Act).

If the Act is passed by the Dutch Parliament and enters into force, any such contractual clauses will be null and void.

What are the policy objectives?

The Act aims to stimulate the growth and development of smaller businesses.

Smaller businesses commonly assigned or pledged their receivables to a lender, who might then lend them up to 80% of the value of such receivables. This assisted them with raising capital for growth. However, other parties contracting with SMEs have begun to insist on barring such assignments or pledges, making invoice financing a near-impossibility for smaller traders.

The Act will counter this recent practice, making it easier once more for SMEs to raise capital.

Current law

In principle, under Dutch law, the ownership of receivables is transferable, unless the law or the nature of the receivable prevents a transfer. Contracting parties are therefore free to determine the parameters and limitations of such receivables.

Exclusively for receivables, s3:83 paragraph 2 of the Dutch Civil Code (DCC) determines that their transferability can be prohibited contractually. If a contract prohibits the transfer of receivables, then they can neither be transferred nor pledged.

A transfer contrary to such clause will, depending on the exact wording of the clause and its interpretation, result in a default (under contract law) or the non-transferability of the receivable, and thus the invalidity of any attempted transfer or pledge (under property law).

To stimulate the provision of loans to SMEs, the Dutch legislator intends to amend s3:83 of the DCC.

The Act states that the transferability or pledging of a business’s receivables can no longer be contractually excluded. Any such clause will be null and void. The expectation is that this will increase the credit potential of borrowers, enabling them to use these receivables as security for their borrowings.

Any transfer or pledge of receivables arising from a business or profession must be in writing. Furthermore, notification of transfer or pledge to the third party (debtor of the receivable) must also be in writing. These latter requirements are not particularly onerous, since written agreements are the norm in international financing practice.

The amended s3:83 of the DCC will not only apply to new agreements but also to existing ones, as from three months after the Act comes into force.

The legislator intends to include several exceptions to the new rule. The following receivables are excluded and may therefore still be subject to transferability and pledging restrictions:

- receivables arising from a current or savings account

- receivables arising from syndicated loans

- receivables from or on a clearing institution, centralised counterparty, settlement agent, clearing institution, or central bank, and

- pecuniary claims which are to be paid on the basis of an agreement as referred to in s34(3), s35(5) or s35a(4) of the Collection of State Taxes Act 1990 into a bank account held for the payment of wage tax, turnover tax and social insurance contributions.

As noted above, receivables arising in the context of syndicated loans concluded on standard LMA documentation will not fall within the scope of the new rule.

The ability to provide collateral for credit facilities should boost lending sources for SMEs and provide a much-needed stimulus for growth.

Find out more

To discuss any of the issues raised in this article in more detail, please contact a member of our Banking & Finance team.

Latest insights in your inbox

Subscribe to newsletters on topics relevant to you.

Related Insights

A new dutch environmental act: what are the consequences for real estate finance.

by Andrei Babiy and Paul Orij

ESG in the Dutch banking sector

- Campaigns and online tools

- Media centre

- Data protection & privacy policy

- Cookie policy

- Legal and regulatory information

- Regulatory information on costs

- Complaints procedure for clients

- Terms of use

- Anti-slavery statement

- Environmental

- Scam emails

© Taylor Wessing

COMMENTS

Being of the opinion that the adoption of uniform rules governing the assignment of receivables would promote the availability of capital and credit at more affordable rates and ... the law governing the original contract is the law of a Contracting State. 4. The provisions of chapter V apply to assignments of international receivables

the resulting "applicable law" may be different to that which Rome I would prescribe). For reference, the US has recently ratified the UN Convention on the Assignment of Receivables in International Trade which, amongst other things, sets out certain conflict of laws rules in relation to the assignment of receivables. For

Receivables finance or also called accounts-receivable financing is a type of asset-financing whereby a company uses its receivables as collateral in receiving financing such as secured short-term loans. In case of default, the lender has a right to collect associated receivables from the company's debtors. In brief, it is the process by ...

Assignment of receivables would mean sale of the lease rentals, not the asset. In that case, the leased asset still remains the property of the assignor - that is, the assignor has retained the residual interest in the asset. However, it would be different if the lessor sells the asset that has been leased out.

With no visibility on whether receivables had been previously assigned, a notice of an assignment serves as an important basic risk mitigant towards double financing. In addition, in cases of multiple assignments done by the supplier, a notice serves to give priority to a funder against subsequent funders - this can make all the difference if ...

Assignment of Receivables. The Transferor will take no action inconsistent with the Purchaser's ownership of the Receivables. If a third party, including a potential purchaser of the Receivables, shou...

The validity of an assignment of receivables cross-border depends on the law that applies to the assignment. What might amount to a valid assignment in one jurisdiction, does not mean, that it is ...

Assignment of receivables would mean sale of the lease rentals, not the asset. In that case, the leased asset still remains the property of the assignor - that is, the assignor has retained the residual interest in the asset. However, it would be different if the lessor sells the asset that has been leased out.

assignment of government receivables. Upon request by the Bank , the Borrowers will cooperate with the Bank in executing any assignment, claim, agreement, document or instrument required or permitted by any governmental unit (federal, state or local) to permit the registered assignment of payment of Receivables to the Bank, including compliance ...

Law on assignment of receivables: Swiss conflict of laws rules As a general rule under Swiss conflict of laws rules, the transfer and assignment of a receivable will be governed by the law governing such receivables. However, the Swiss Private International Law Act of 18 December 1987 (PILA) allows for a choice of law (ie, a law other than that ...

Historically, this had been viewed as something of a 'grey' area of the law - governed in a piecemeal way, with Federal Law No. 5 of 1985 (as amended, the Civil Code) governing the assignment of ...

Abstract. This article describes the conflict-of-laws rules of the USA and Canada on the effectiveness against third parties and priority of an assignment of trade receivables. Comparisons are ...

factoring industry", the legal framework governing assignment of receivables is mainly laid out in China Contract Law. I. Receivables That Can be Assigned Article 79 (Assignment of Rights; Exceptions) of China Contract Law reads: ... So it is certain under Chinese laws that once assignment of receivables is effected, then the title in the ...

From a Swiss legal perspective, in order to ascertain the enforceability of an assignment against a debtor of receivables, the assignment of a receivable must be subject to the law governing the ...

In particular, in its response to The Business Contract Terms (Assignment of Receivables) Regulations 2017, The City of London Law Society (CLLS) noted that prohibitions and restrictions on assignment (including assignment of receivables) are common in construction contracts, such as the JCT suite of contracts, because developers wish to ensure ...

The validity of an assignment of receivables cross-border depends on the law that applies to the assignment. ... in which case the law governing the account or the financial instrument will apply ...

Assignment of Receivables. 3rd November 2017. The draft Business Contract Terms (Assignment of Receivables) Regulations 2017 (the " Draft Regulations ") are currently before Parliament. If approved, these would contain provisions to nullify contract terms which attempt to restrict the ability of a party to assign a receivable.

that the adoption of uniform rules governing the assignment of receivables would promote the availability of capital and credit at more affordable rates and thus facilitate the development of ... debtor is located in a Contracting State or the law governing the original contract is the law of a Contracting State. 4. The provisions of chapter V ...

Related to ASSIGNMENT OF RIGHTS AND RECEIVABLES. Assignment of Rights Borrower acknowledges and understands that Agent or Lender may, subject to Section 11.7, sell and assign all or part of its interest hereunder and under the Loan Documents to any Person or entity (an "Assignee"). After such assignment the term "Agent" or "Lender" as used in the Loan Documents shall mean and ...

Assignment of receivables is ubiquitous - it is there in whole lot of financial transactions - securitization, loan sales, factoring, sale of non-performing ...

Ottawa Convention was indeed the model for the final draft. Under § 354a HGB, the assigned claim does not fall under the estate of the assignor and is transferred to the assignee's estate; the assignment is "absolutely" effective. However, the creditor may still pay to the assignor and thereby discharge his debt.

Current law. In principle, under Dutch law, the ownership of receivables is transferable, unless the law or the nature of the receivable prevents a transfer. Contracting parties are therefore free to determine the parameters and limitations of such receivables.

1. This Law applies to transfers of receivables. 2. Nothing in this Law affects the rights and obligations of a person under any other law governing the protection of parties to transactions made for personal, family or household purposes. 3. Nothing in this Law overrides a provision of any other law

Subtopic 310-40, Receivables- Troubled Debt Restructurings by Creditors. To be an eligible loan modification under Section 4013, as amended by the Consolidated Appropriations Act, 2021, a loan modification must be (1) related to the Coronavirus Disease 2019 (COVID-19); (2) executed on a loan that was not more than 30 days past due as of

The validity of an assignment of receivables cross-border depends on the law that applies to the assignment. What might amount to a valid assignment in one jurisdiction, does not mean, that it is valid in another and where there are competing claims to the receivables and competing jurisdictions, the question of which law applies and therefore whether there has been a valid assignment ...

These inter-fund receivables and payables are expected to be repaid in with ... created by resolution of the governing board, without voter approval, provided that the ratio of the ... shall be applied first to the assigned fund balance to the extent that there is an assignment and then to the . unassigned fund balance. W) Implementation of New ...

London Stock Exchange | London Stock Exchange ... null